As we were moving into 2023 earnings, I was expecting to start seeing the top leaders moving ahead. But, to my surprise, things got more complicated instead.

As if interest rates, supply constraints, sticky inflation, and an ongoing war weren’t enough. We got several (3 to be exact as of this writing) banks collapsing in a matter of days.

And this is why, when it comes to investing, it’s easy to get caught up in the numbers. But as the latest earnings reports show, there’s a lot more to investing than just dollars and cents.

So, I guess just like other investors, I have many questions including:

- Are CEOs just blaming macro or are they really slowing down significantly?

- Are they being prudent or is this just the new reality?

- Should we be expecting a significant turnaround any time soon (if ever)?

- Are multiples fair at current levels or are we gonna see rerating if inflation remains sticky and hence all the headwinds remain for the next few quarters?

In other words, when are we gonna make some money?

These are some of the questions I’ll try to answer today while also providing:

- General thoughts on the market

- My take on the latest earnings reports

- Recent trades and portfolio allocation

These are my own thoughts and are presented in an attempt to help me (or anyone else reading) put my (or your) thoughts in order. Once I put something to paper it becomes a bit clearer.

All these initial views are taken without reading comments from others in order to keep them as original as possible and avoid echoing others (or changing opinions based on others before even giving me the chance to digest info on my own).

What you'll learn:

⓵ General thoughts on the market

❖ Inflation

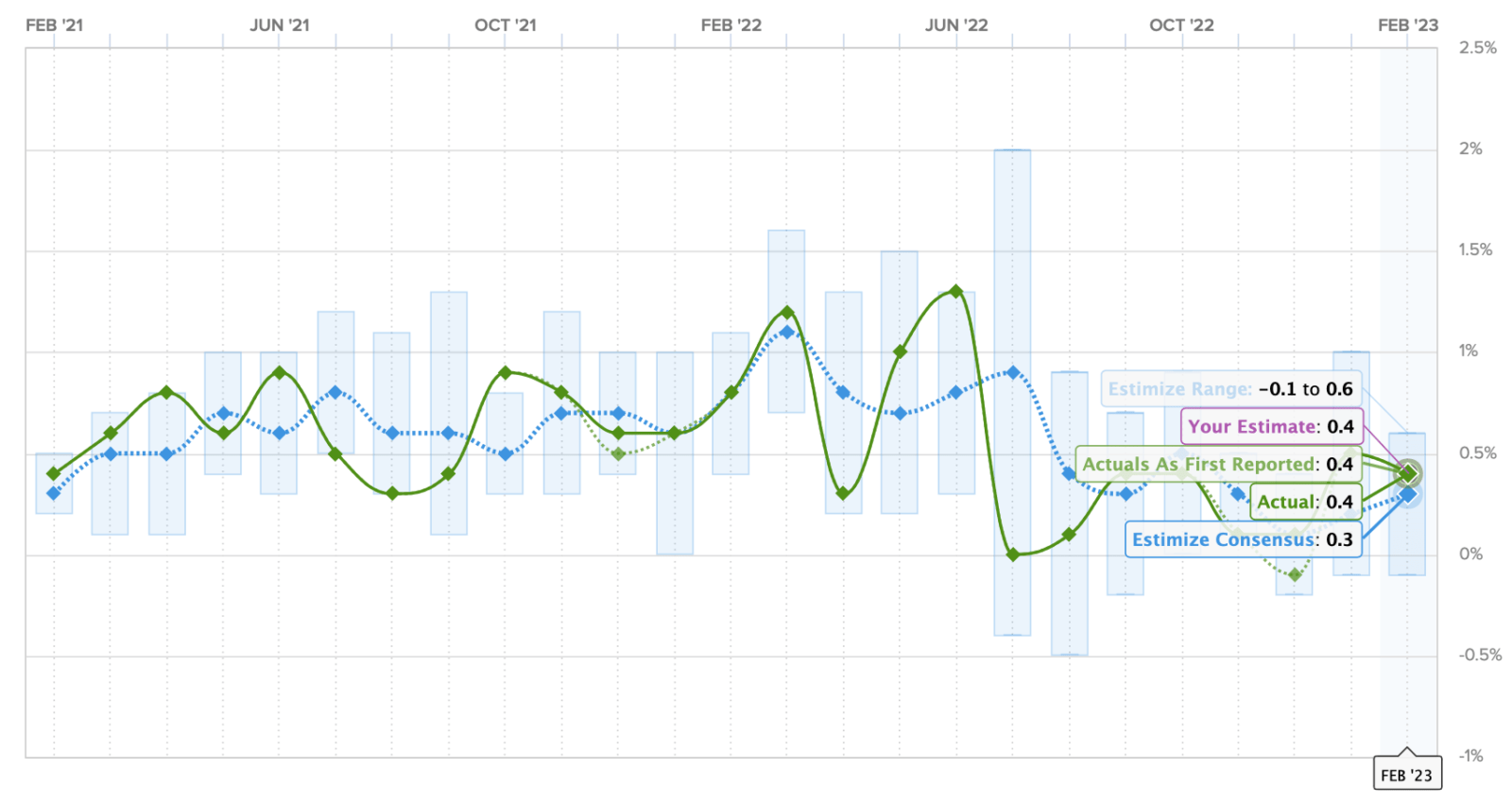

Inflation concerns are still valid (still growing 0.4% MoM) as anticipated.

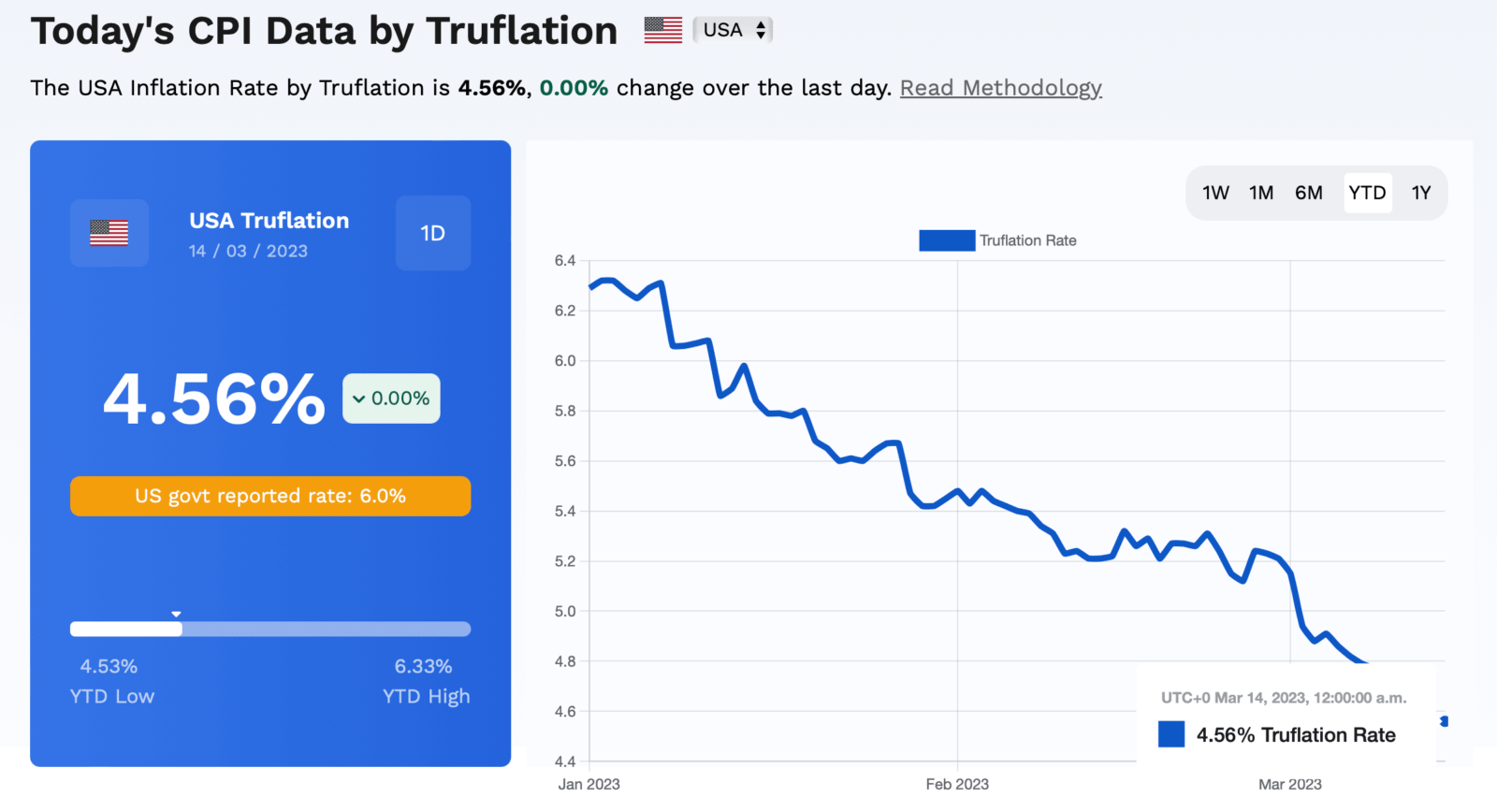

This annualizes to 6% which is what the Fed is reporting. However, truflation shows 4.56% instead as they use several data sources instead of annualizing the latest MoM one. You can see the dashboard for all categories here.

The Fed is not trying to achieve deflation (revert inflation). But disinflation instead (slow the pace at which inflation is increasing).

Almost every company (no matter how big or small — from hyperscalers down to small players) has felt the impact.

Clients try to optimize (cut expenses). They scale slower. And try to become more efficient in their spend. Also, they don’t go all in on their new contracts. But take their time to ramp up instead.

❖ Hiring

Hiring stopped (for some). Others reduced staff (ZS). While others are still hiring (SNOW).

Everyone says that cutting staff is smart in this environment. Now I don’t know whether that’s smart or not. But if they overhired during covid where demand was strong, then yes. If you no longer need the extra help then it makes sense.

But if you have plans and strong demand, then now is the time to steal top talent.

Why?

Because options (for applicants) are limited. People get fired left and right. What this means is that top talent is out there. Available. Waiting for forward-thinking companies to reach out.

And this is why I understand that it makes sense to cut staff. But I also understand why Snowflake keeps hiring (1000 new adds for this year).

❖ SBC

When it comes to Stock-Based Compensation (SBC), everybody seems to hate this lately. In previous years very few (if anyone) ever bothered with it. I understand it dilutes shareholders. I also understand that it’s a necessary evil in an attempt to attract and retain top talent.

As long as companies keep it under control. Either through buybacks (more on this in a sec). Or keeping it under a certain level per year (2-3%). Then it makes sense. I wish I had the chance to be part of a company that offered SBC (but what do I know?).

❖ Buybacks

Buybacks. Another word that raises brows lately. I wish I was smarter than all these CEOs and CFOs who make these decisions. And I could tell you how wrong they are. But I’m not. And I don’t pretend to know what’s best for these companies when it comes to buybacks.

Yes, ideally you would want every growth company to be able to utilize the extra cash to grow even further, innovate, come up with new products (invest in research and development), and try to sell more (through sales and marketing).

But what if at these times none of it will help push the needle?

Would you rather have these companies spend the extra cash on S&M or R&D anyway?

Would that make investors happier?

But what if they are just being prudent? And try to use cash as they see fit. And when the time is right they’ll push for growth. And similarly, when it makes sense, they do buybacks (or whatever they think is good).

So as long as the long-term thesis is intact buybacks don’t bother me. In fact, I kind of like them. Buybacks increase investors’ interest in a company. It’s the opposite of dilution. So if both exist then they kind of neutralize the negative effect (at least this is how my simple mind sees it).

❖ Consumption vs subscription

Few Qs back we saw that consumption was superior (with no major slowdown because of macro). Now we see the exact opposite. I’m not worried about consumption models because these companies had strong customer adds nonetheless.

This means that when they start ramping up in the next Qs (or even years) the growth will still be significant. It’s not like they stopped adding new customers. But it’s just that customers decide to go slower than before.

And try to stretch their dollars’ worth by not signing up for multiple years upfront or larger deals in advance. But instead, they prefer to start smaller and scale as they see fit. This is them being prudent in their spend while trying to find the right size of deal for their specific needs.

Onwards.

⓶ My take on the latest reports

❖ SNOW

Expected: $565m (product)

Results: Not that great (lower numbers and lower FY guidance)

Concerns:

- Is the lower guidance just the prudent thing to do or there’s a great impact on consumption?

- Can they really achieve the $10b target or do they just reiterate that to keep investors somewhat happy?

Decision: Added to my position after the drop as I see this as an opportunity for those with a time horizon of longer than a day or two.

Notes from the call:

- 3% beat

- No major slowdown during Xmas holidays

- No major AI growth as of now

- Customers more cautious (hence lower bookings)

- NRR 158% (and slowing down)

- Controlling cost clients still grow

- Financial services biggest sector (then media & technology)

- Large Global 2000 clients grow meaningfully

- Billings not important (focus on revenue)

- Operating margin expands rapidly from FCF (since it’s a much lower number)

- 6% OM and 26% adjusted FCF margin

- Clients still ramping but at a slower pace (cost control)

- Macro and migration

- CFOs trying to cut costs (either through headcount or other things)

- Recent adopters grow but ramp slower (because of macro, trying to be efficient)

- No reduction in use cases (migrations and on-prem data warehouse like Redshift)

- Plan to hire 1000 more people this year (vs 1900 last year)

- Focused on efficient growth vs growth at all costs

- Don’t focus on total number of customers (focus on quality/big ones or small with potential)

- Revenue per customer growing

Risks:

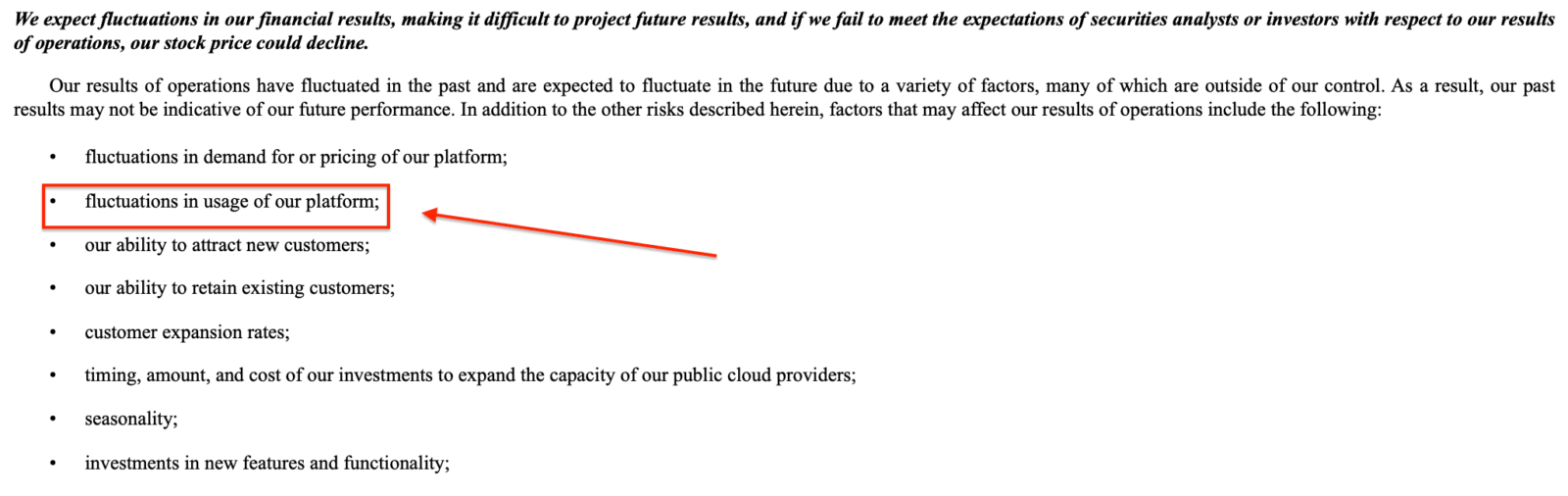

Consumption might make revenue lumpy. Sometimes to the upside (when customers have cheap access to cash) and sometimes to the downside (like now that customers are more prudent with their spending). You can read about all the risks directly from the latest 10-K.

Bulls vs Bears:

| Bulls say: | Bears say: |

| Could remain the only multi-cloud offering for much longer than anticipated (thus increasing its revenue with minimal pricing pressure). | Other multi-cloud data competitors may emerge or in-house data warehouses at AWS or Azure could potentially adopt a multi-cloud strategy |

| Could move to a subscription model (and boost monetization of its products) | Fail to expand its data-sharing network extensively (leaving it vulnerable to competition with larger networks) |

| Could expand to other multi-cloud data needs (and push spending per customer higher) | Migration of existing workloads to the cloud could occur at a slower pace (and extend the length of unprofitable years ahead) |

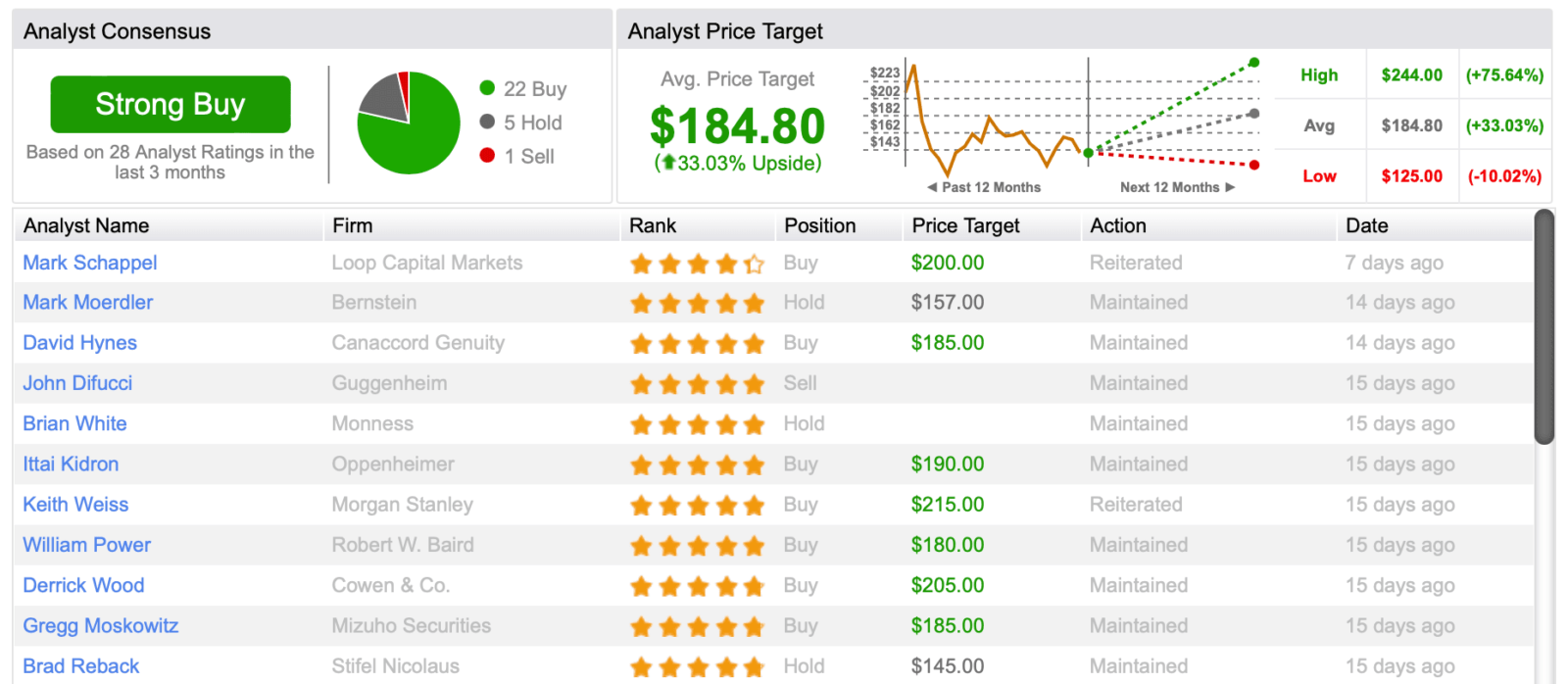

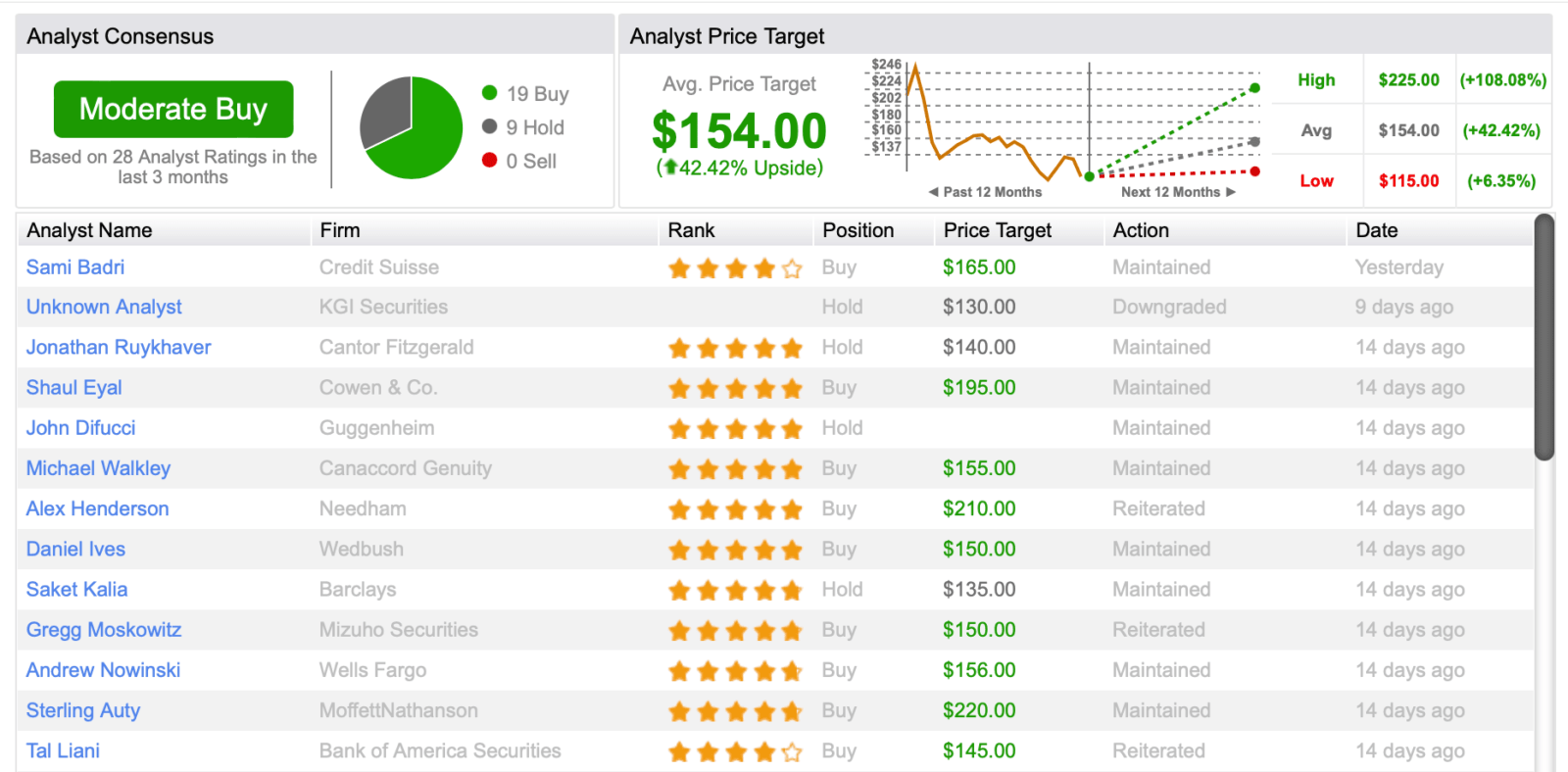

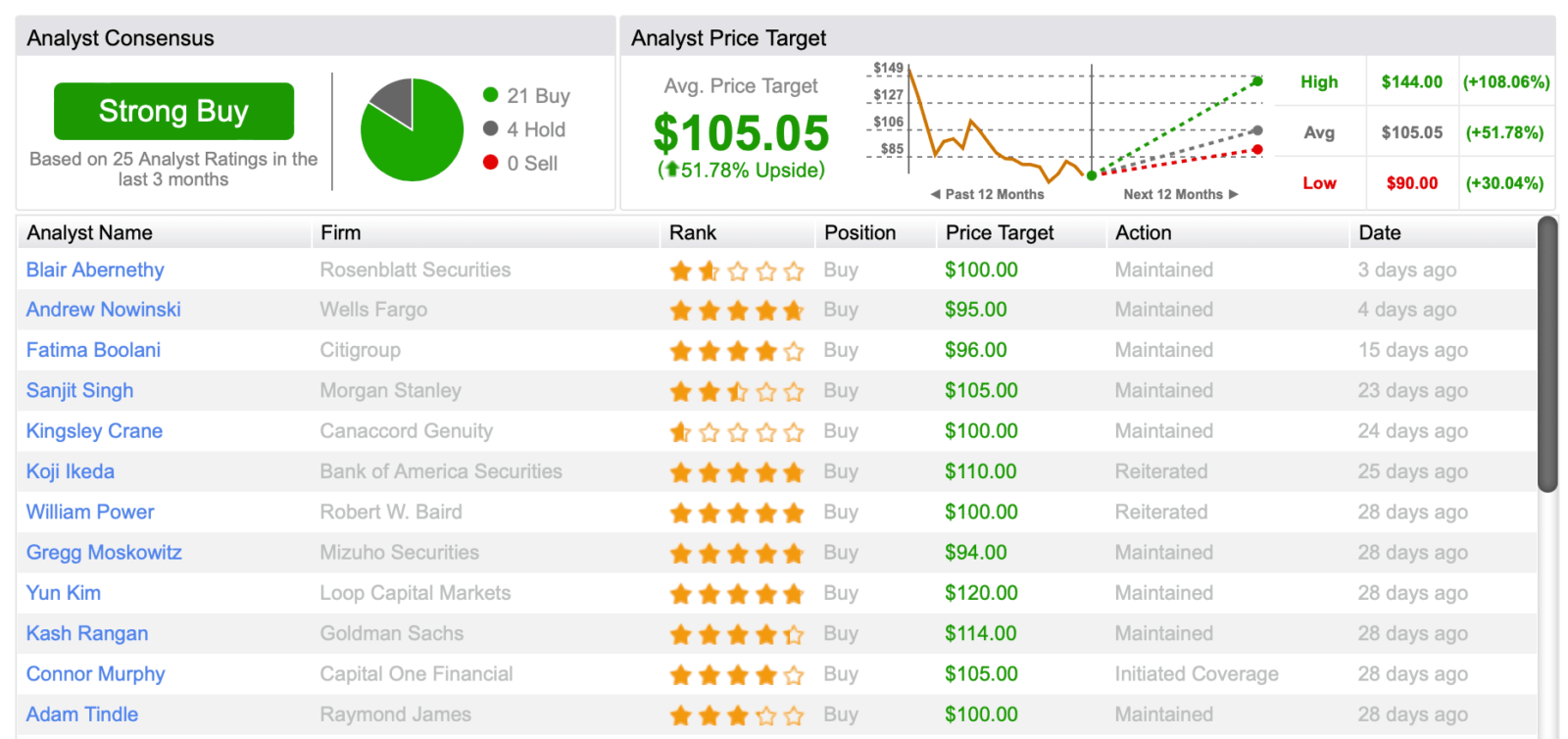

Analyst estimates:

Technicals:

So far there’s been good support at around 120. However, if subsequent quarters deteriorate, there’s a big chance of dropping below that. For now, it seems there are plenty of buyers at that level. Time will tell.

❖ ZS

Expected: $380m

Results: Very good numbers, lower billings

Concerns:

- Will lower billings affect revenue as much even though management says don’t look at billings for the time being?

- When will delays in large deals ameliorate?

Decision: Added after the drop as I believe the market is mispricing the effect of billings into the future prospects of the company

Notes from the call:

- Customers more cautious with billings in advance (can be irrelevant looking at billings for now)

- Delays in large deals (not gone away)

- Ramp up slower (in the second year)

- Cybersecurity remains top priority

- Better multi-tenant architecture over smaller vendors

- Balance growth and profitability

- Additional approvals needed (because of trying to save costs)

- Customers like consolidation with clean architecture (give strong ROI to clients)

- Almost all new business replaces something else

- Billings would be different (couple of percentage points higher)

- Help clients start and then ramp up (in year 2)

About guidance:

- Environment assumed it will continue

- Elongation of sales cycle (slightly worse than Q2)

- Macro impacts high-end deals

- Lower-end deals remain unchanged (contrary to Snowflake which sees the opposite)

- Money comes from: 60% upsell, 40% new deals

- Increased scrutiny from CISOs

- Aren’t seeing pressure on discounting (some clients do it)

- One of the most critical solutions for clients

- Q4 billings need to be higher as Q3 billings will take a hit (-9% as per management)

- Not incentive for new logos

- Want expansion (upsell) easier than new logos (for now)

- Customers rave about them (best service, architecture, security)

- Opportunity to upsell data protection

- Revenue is a lagging indicator

Risks:

Taken directly from the latest 10-K.

Bulls vs Bears:

| Bulls say: | Bears say: |

| Strong tailwinds as the convergence of networking and the security market is in its early innings | Large public cloud vendors often offer their own cybersecurity solutions (and could hinder growth opportunities) |

| Market leadership and high enterprise penetration through its offerings related to secure web gateways and zero-trust network access | Competitors like Palo Alto and Fortinet (and even Cloudflare now) have made investments in the key areas where Zscaler has a market-leading position |

| Consolidate security vendors (because of the wide array of solutions across an enterprise’s network security stack) | Xara May miss out on the next big technology (and allow its competitors to catch up) |

Analyst estimates:

Technicals:

❖ BILL

Expected: $255m

Results: Solid numbers, bad next Q guidance

Concerns:

- Is the negative QoQ guidance because of usual seasonality (and being prudent) or are we going into negative numbers moving forward?

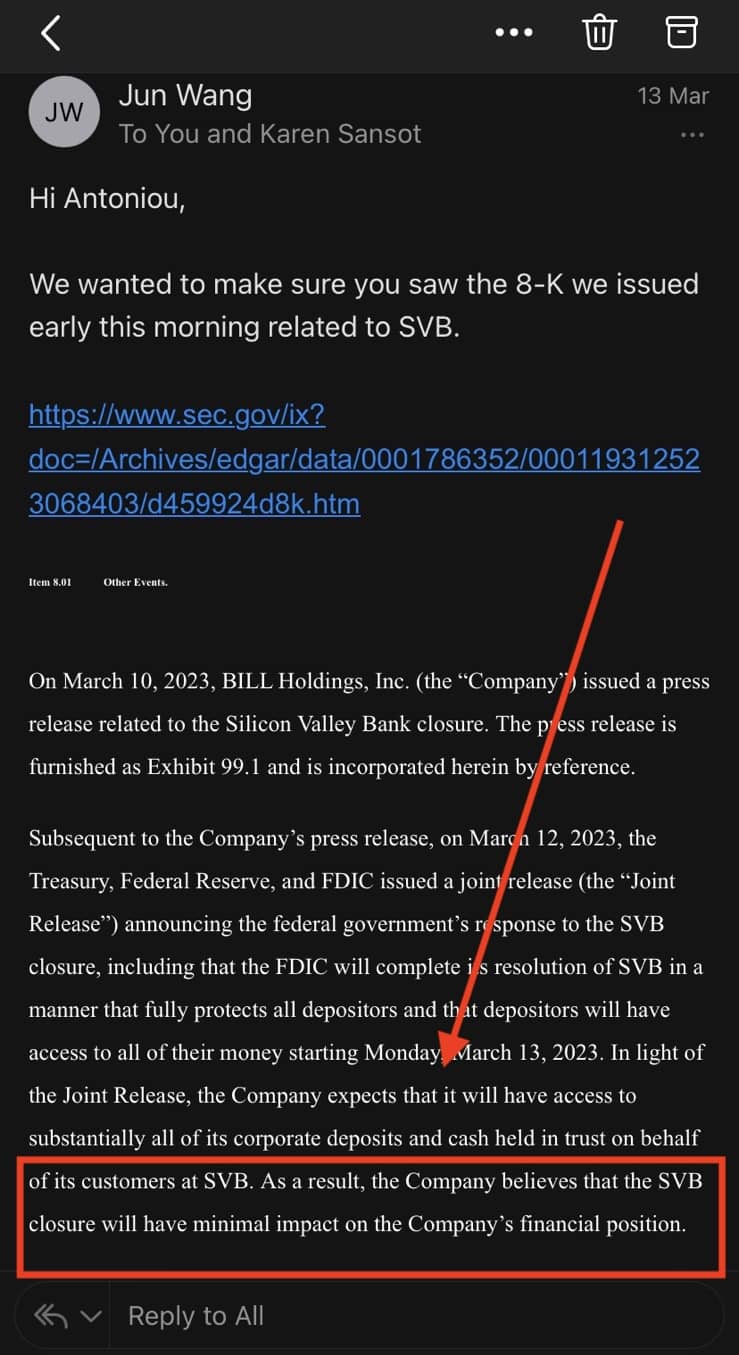

Decision: Added after the SVIB collapse once the IR confirmed that all depositors will be backed

Notes from the call:

- 6000 accounting firms/partners

- Gross margin expansion and profitability

- 86.7% highest GM on record

- $48m in FCF

- Float revenue higher because of rising rates

- SMBs on stand-by mode, try to manage their spend (hence TPV lower)

- Balancing NG profitability

- Spending pattern changes

- Core net customer adds ticked lower than 5000 (excluding FI channel

- Macro and seasonality affecting TPV guidance for Q3

- Balance growth and profitability

- Increased NG profit by 10%

- Even with float removed, gross margin very healthy

- FI channel contributing over half of net new adds

- Long-term opportunity ahead

- Guide impacted by TPV

Risks:

Even though Silicon Valley Bank exposure is not going to have any significant impact on Bill’s business (as per management), this might be a key risk for something similar in the future. Also, Intuit said they are increasing their own platform’s capabilities which is noted as a risk on Bill.com’s 10-K.

Bulls vs Bears:

| Bulls say: | Bears say: |

| Lot’s of greenfield opportunities ahead | Too complicated to follow |

| Higher interest rates benefit float | Based on acquisitions |

| Deflationary product | Doesn’t deserve a hefty premium |

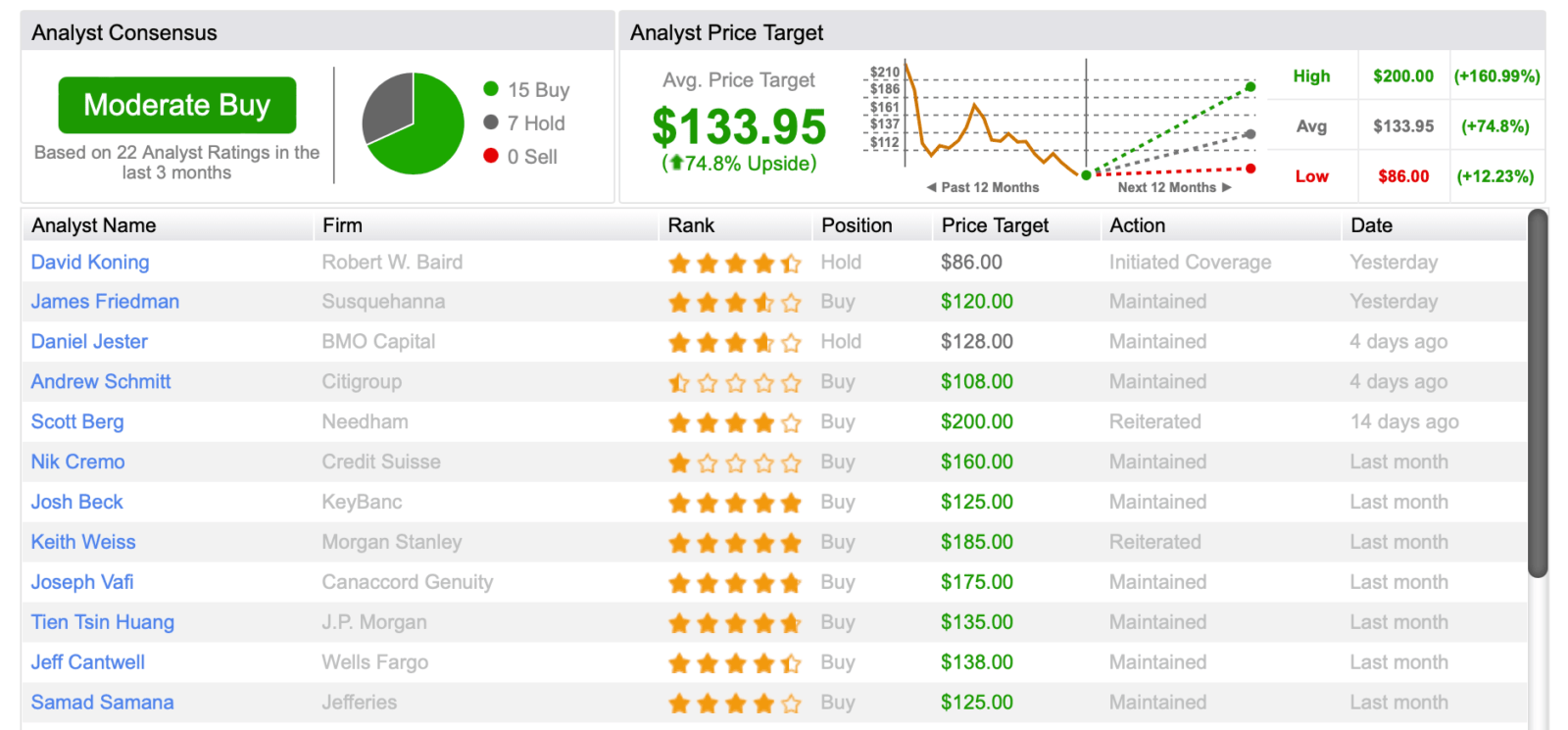

Analyst estimates:

❖ DDOG

Expected: $465m

Results: Good numbers, slowing growth

Concerns:

- Is the company really slowing that much or are they just being prudent like everyone else?

Decision: Added when the price started dropping below $70

Notes from the call:

- Guiding 25% of growth next year

- 21% FCF margin

- DBNRR still above 130% (22nd time)

- Slower usage growth from big customers

- Larger spending customers seasonal annual slowdown as previous years

New logos:

- Insurance company

- Federal agency

- Japanese hardware

- Clients more cautious short term but long term stays intact

- Balancing long-term investments while macro remains uncertain

- Discipline growth over 2023

- Typical slowdown more pronounced than previous years

- Ecommerce and food delivery bigger slowdown

- Slower duration billing YoY

- 81% GM up from 80%

- Lower growth trajectory for Q1

- 20% growth of headcount (vs 50% previous year)

- No change in long-term opportunities

- Similar trend like hyperscalers (not 1:1 though)

- Cloud migration/digital transformation headwind over next Q but tailwind again in the future but can’t tell when exactly (hyperscalers can’t say when either)

- Focus on future success

- Several products still in early lifecycle (can be main driver of growth in the foreseeable future)

- Small clients not much of a slowdown (vs big clients)

- Guidance assumes optimization continues

- Not directly related to layoffs in tech but in optimization in cost from clients

Risks:

Taken from the 10-K directly, you can read them all here:

Bulls vs Bears:

| Bulls say: | Bears say: |

| Strong tailwinds as the FSMA market is expected to grow rapidly | Product portfolio currently lacks the comprehensiveness of Splunk’s platform (leading to lost sales in the enterprise space) |

| Additional products (including recent security offerings) can offer different points of entry into potential clients’ IT ecosystems | There is uncertainty about when Datadog will achieve GAAP profitability |

| So far focused primarily on SMBs. Still a big enterprise opportunity ahead | Penetration in the enterprise market lags some of its peers |

Analyst estimates:

Technicals:

❖ CRWD

Expected: $365

Results: Great numbers and guidance

Concerns:

- Did they take talent from S because they feel the pressure or was it just because S decided to eliminate the role?

Decision: Added to my position at around $118

Notes from the call:

- Exceeded management’s expectations (mine too)

- Rule of 81 on a FCF basis

- Record numbers (net new ARR 12% QoQ, net new customers, FCF, operating income)

- Reiterating ending ARR to $5b by FY26 end

- Reach target operating model in FY25

- Strong market demand (albeit elongated sales cycle)

- Revenue through channel partners (now 83% of revenue)

- Massive SMB opportunity (Daniel Bernard as Chief Business Officer leading this from SentinelOne)

- Raj Rajamani joins from S too as Chief Product Officer for data, identity, cloud, and endpoint (taking staff from S means they are doing something good too, right?)

- Magic number 1.1 (indicating efficient and sustainable sales and marketing efficiency)

- Record Q1 pipeline

- IDC’s modern endpoint security market share — 17.7% (massive amount of legacy technology that’s out there), up by 3.8 percentage points (more share gain than any other vendor, including outpacing Microso)

- GM going down to 75% from 76% (mostly because of cost of data centers, Humio acquisition) next Q to be up by 1% but long term intact to reach 82%+

- Balance growth and profitability (even at scale)

- Moderating the pace of hiring for this year

Risks:

You can read all the risks from the 10-K here.

Bulls vs Bears:

| Bulls say: | Bears say: |

| Strong tailwinds given that the endpoint security market is projected to grow rapidly | Large public cloud vendors often offer their own cybersecurity solutions, which could hinder growth opportunities |

| Market leadership in endpoint security and has high enterprise penetration within the space | Competition from vendors like Palo Alto (and now S) that have increasingly made investments in the endpoint security space |

| Benefits as clients consolidate vendors and opt for a platform-based cybersecurity approach | May miss out on the next big technology, hence allowing its competitors to catch up |

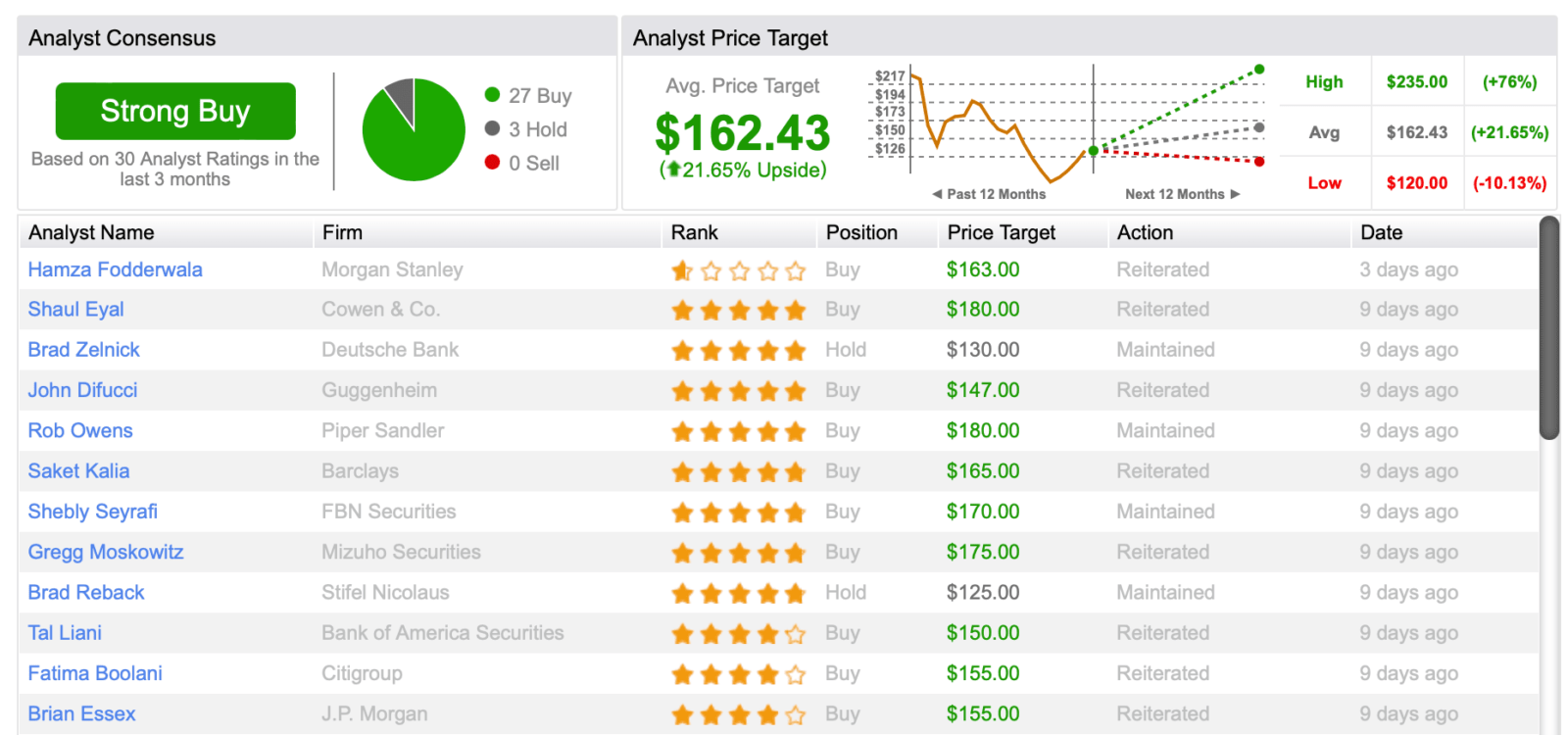

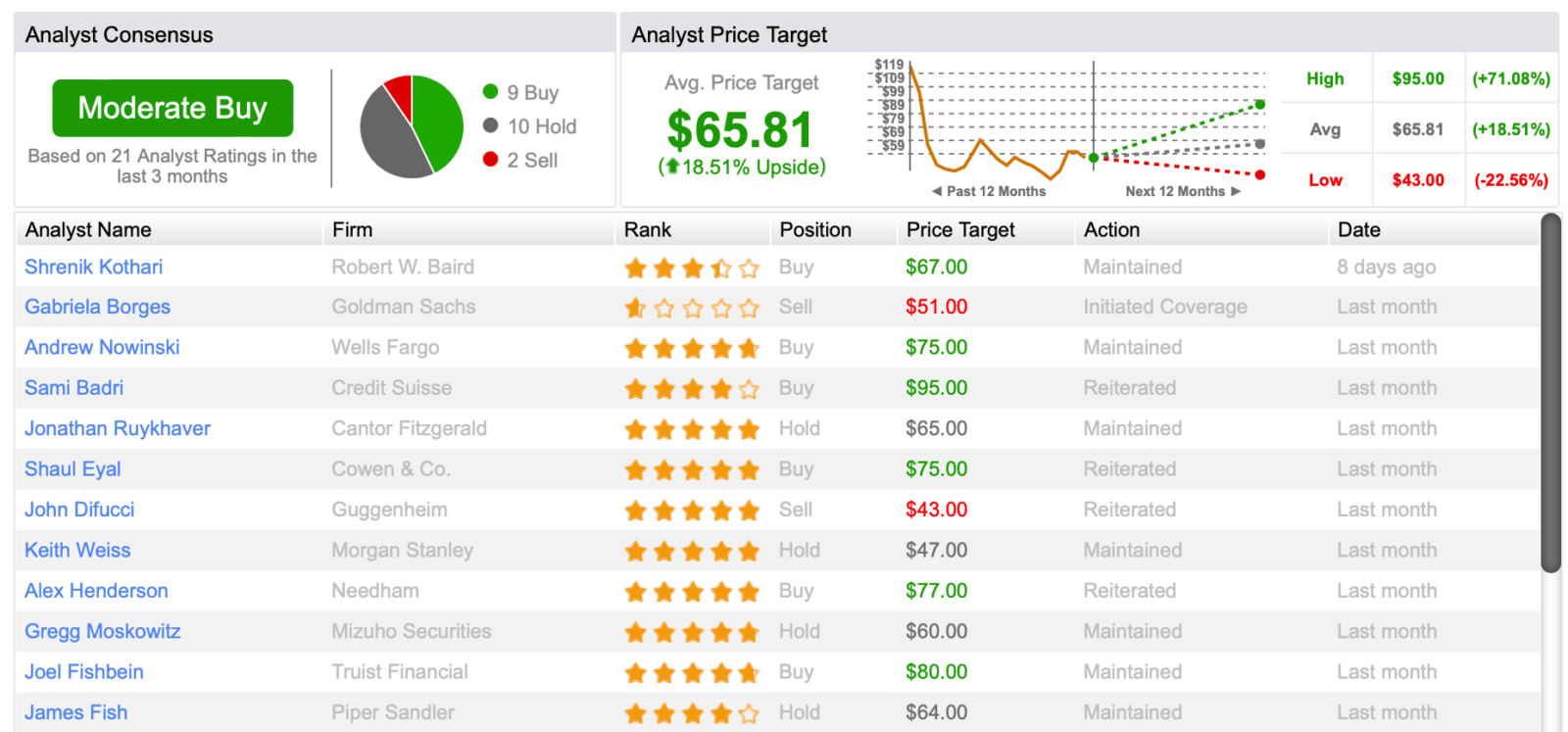

Analyst estimates:

Technicals:

❖ S

Expected: $128

Results: Very good

Decision: Added to my position

Concerns:

- Can they achieve profitability as planned by FY25?

- How much can they beat the 51% YoY guide?

Notes from the call:

- Non-GAAP profit margin improvement (currently 75% vs 66% a year ago vs 71% last quarter)

- Macro remains consistent (longer sales cycles and deal rightsizing)

- Crossed half billion ARR

- ARR up 12% sequentially vs 11% for the prior Q (Q4 $548.7m vs Q3 $487.4m vs Q2 $438.6m)

- Record net new ARR ($61.3m vs $48.8m for the prior Q)

- Major industry valuations (MITRE, Gartner Magic Quadrant, and top-ranking in each Gartner critical capabilities for endpoint protection)

- Rule of 50

- NG operating margin keeps improving (currently at -35% vs -43% prior Q vs -66% last year)

- 100K customers up 74%

- Several multi-million wins in the quarter

- Net expansion (DBNRR) still above 130%

- Cloud security 15% of quarterly ACV and doubled sequentially

- Replaced a competitor for a global internet platform in a multimillion deal (because of architectural shortcomings in the competition)

- Partnership with Wiz (allow customers to get more comprehensive cloud protection)

- Microsoft win (broader coverage from single platform)

Road map focused on:

- Advancing leadership in endpoint security

- Strengthening cloud security advantage

- Expanding platform capabilities and market opportunity

- 51% next year guide and 8.6% QoQ

- Achieve profitability by 2025

- Continue to improve operating margin in FY24 (between -29% and -25%)

- Decided 2 Qs ago to consolidate CPO and CTO under Rick Smith (is this why CPO went to CrowdStrike? Or is this just a cheap explanation?)

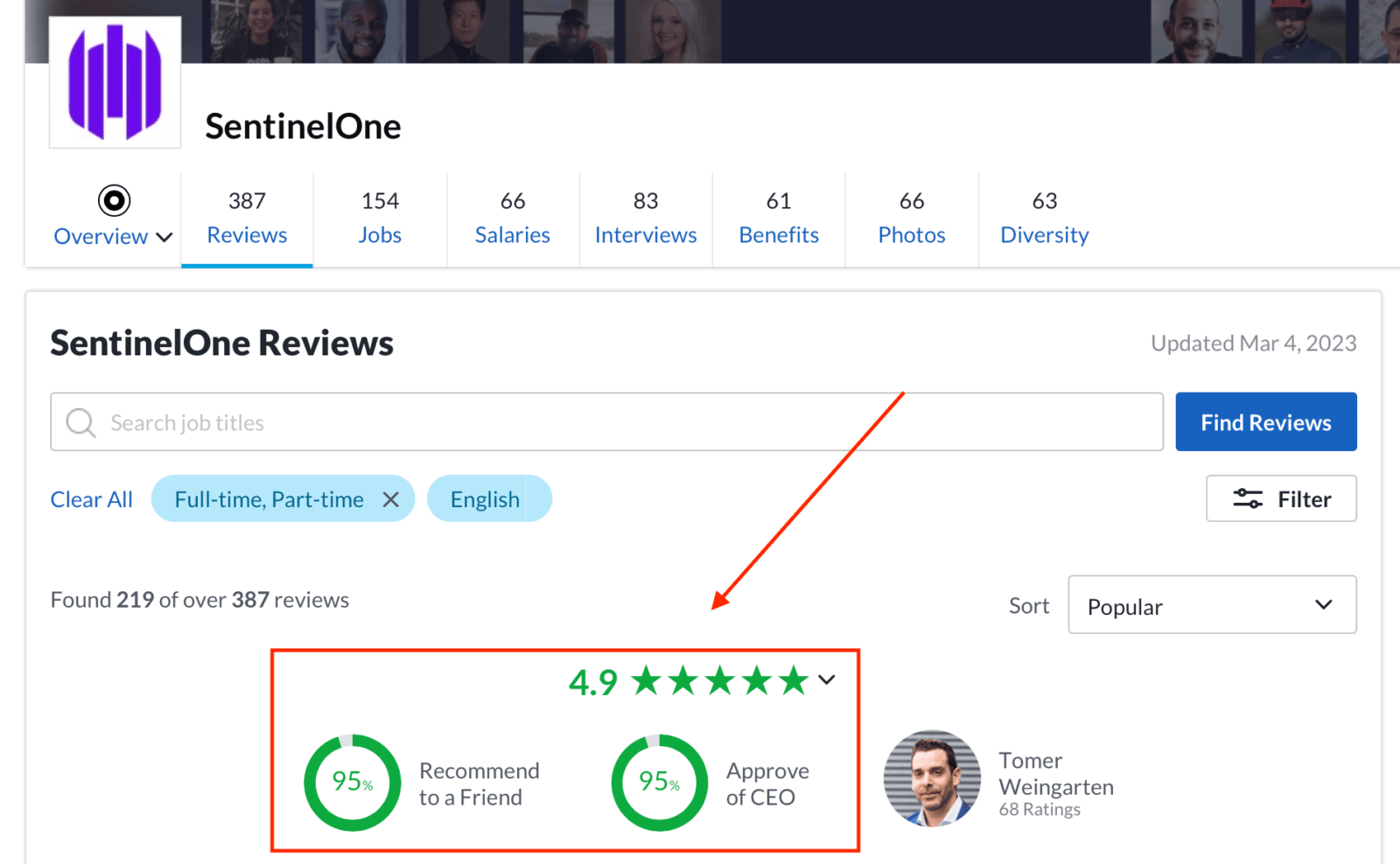

- Glassdoor score 4.9/5

- Healthy mix of new customers and existing customer expansion

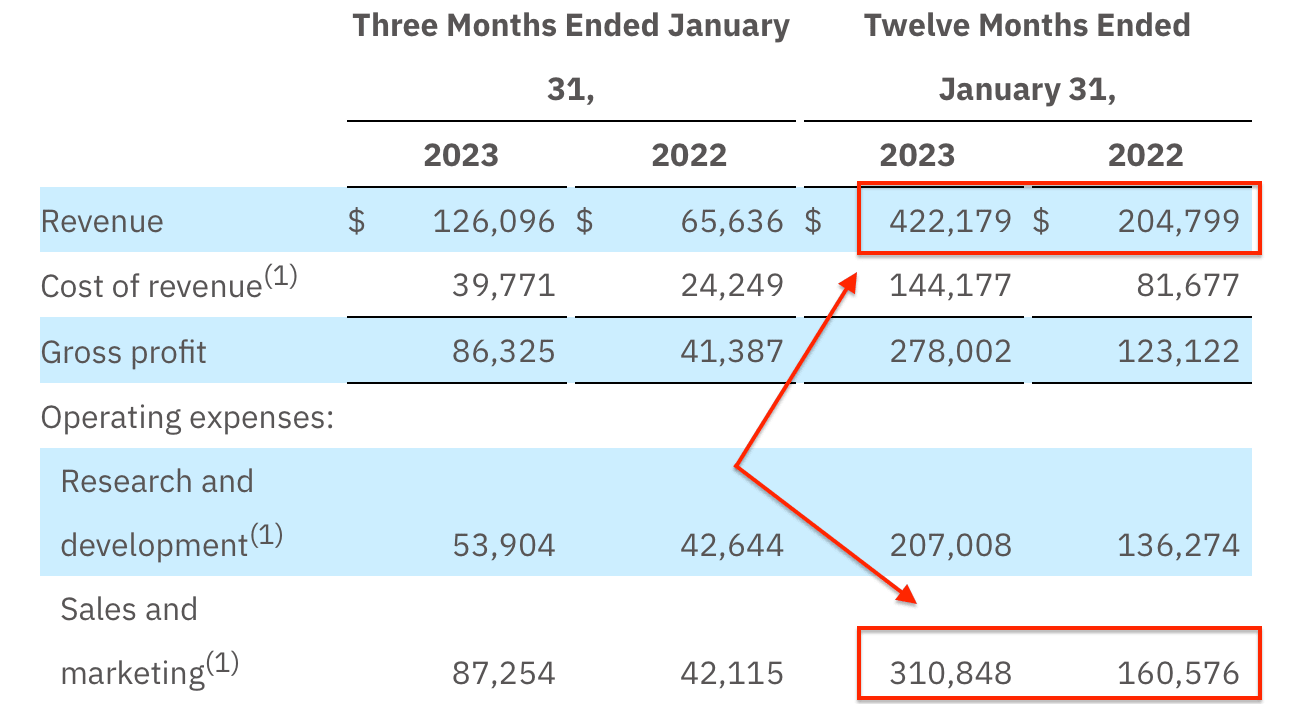

- S&M up 93% in 2023 while total revenue up 106%

- S&M 73% of total revenue (vs 78% for prior year) — still too high compared to peers

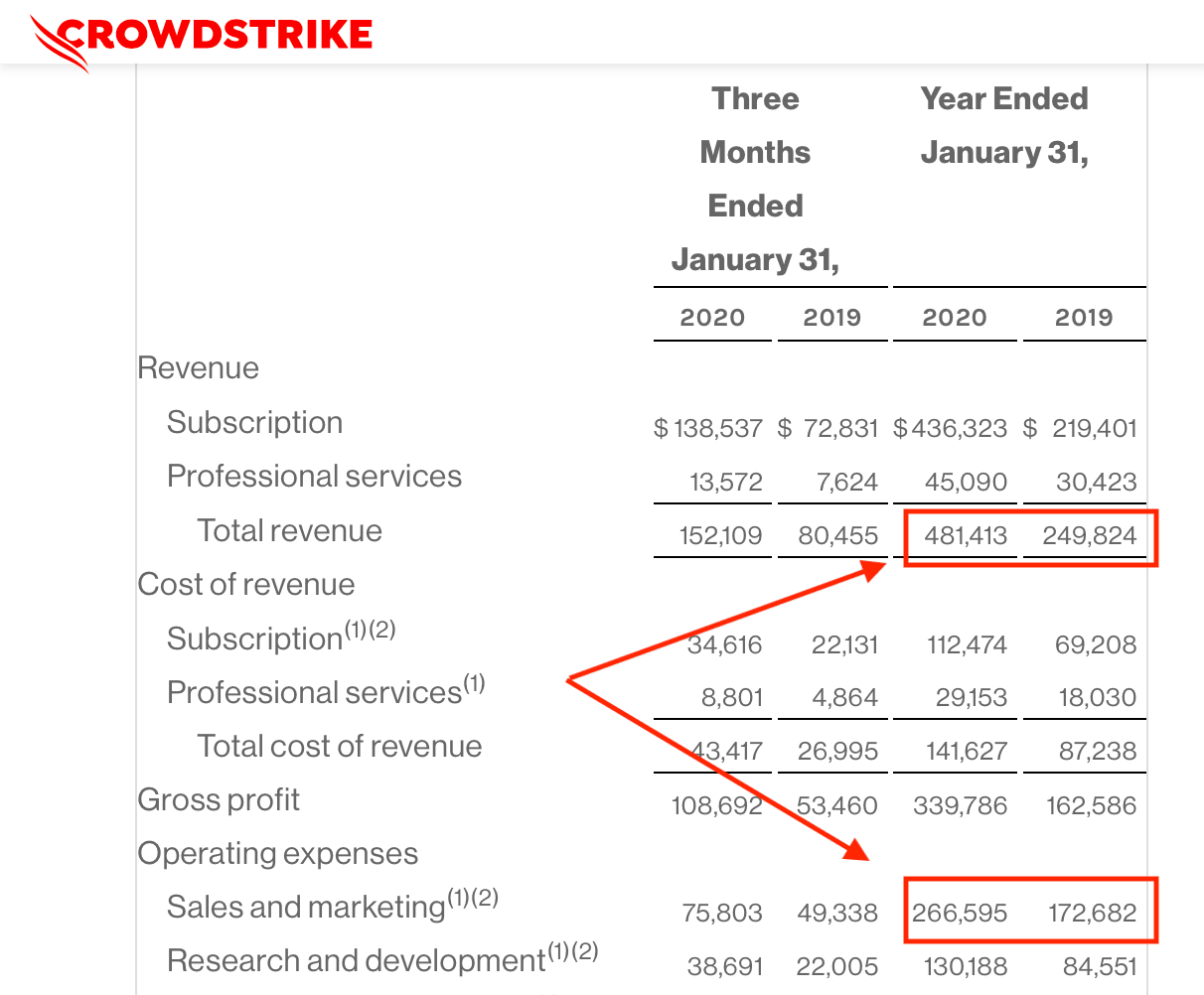

Here’s CrowdStrike’s (55%) when it was in the same phase (albeit SentinelOne is growing amid competition and macro headwinds)

Nevertheless, their magic number is 1.7 which indicates efficient S&M spending (for every $1 they spend on S&M they add $1.7 in ARR).

Here’s how I calculate the magic number:

☞ (ARR FY23 – ARR FY22) / (S&M FY23 – S&M FY22) or 256.4 / 150.3 = 1.7

- Payback time is around 31 months (if my calculations are correct)

Here’s how I calculate payback period:

☞ (S&M spend in previous Q) / (current Q revenue – previous Q revenue) x GM

or

83.9 / (126.1 – 115.3) x 75% = 10.3 Qs (x3 = 31 months)

- $1.2 billion in cash and no debt

- Positive FCF by end of year (subject to global economic conditions)

- Prudent guidance (like so many others)

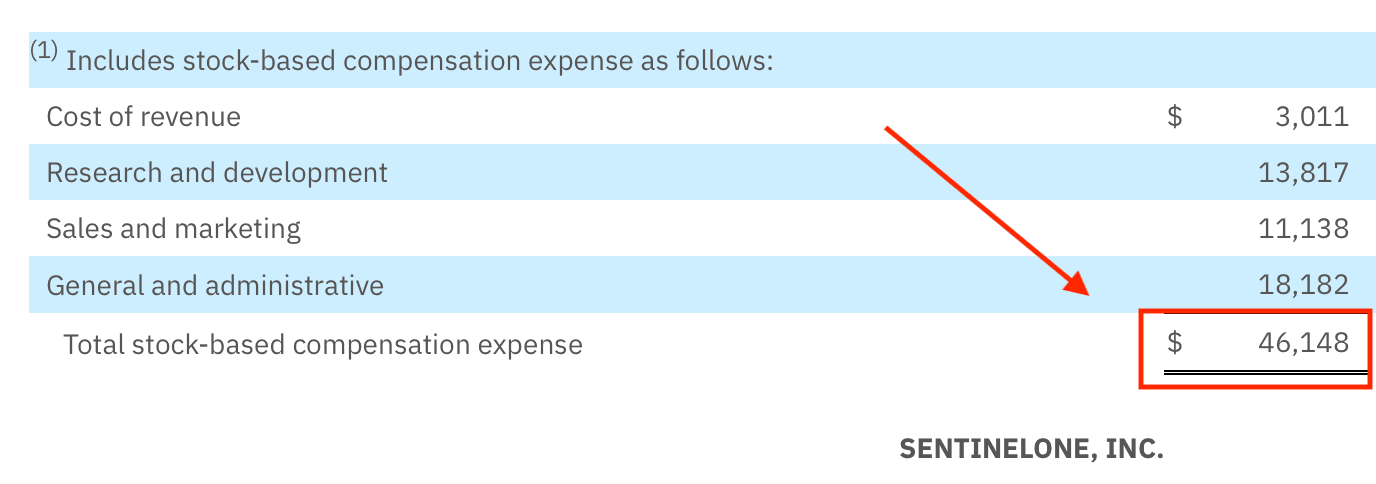

- High SBC

- New CMO will come but CPO role eliminated

- Enterprise sales (shifting messaging to target high-end market)

- More and more focus on EMEA

- Pipeline doubled

Risks:

Here are the summary risk factors as found in the 10-K:

Bulls vs Bears:

| Bulls say: | Bears say: |

| Strong tailwinds as the endpoint security market is projected to grow | Large public cloud vendors often offer their own cybersecurity solutions which could slow growth opportunities |

| Singularity platform improves itself over time (reducing customer churn) | Competition from Crowdstrike and Palo Alto Networks that are larger and more well-capitalized |

| Plenty of greenfield opportunities without running into competition against larger players | As the firm puts more cash into its research and sales divisions, investors should not expect positive GAAP operating margins soon |

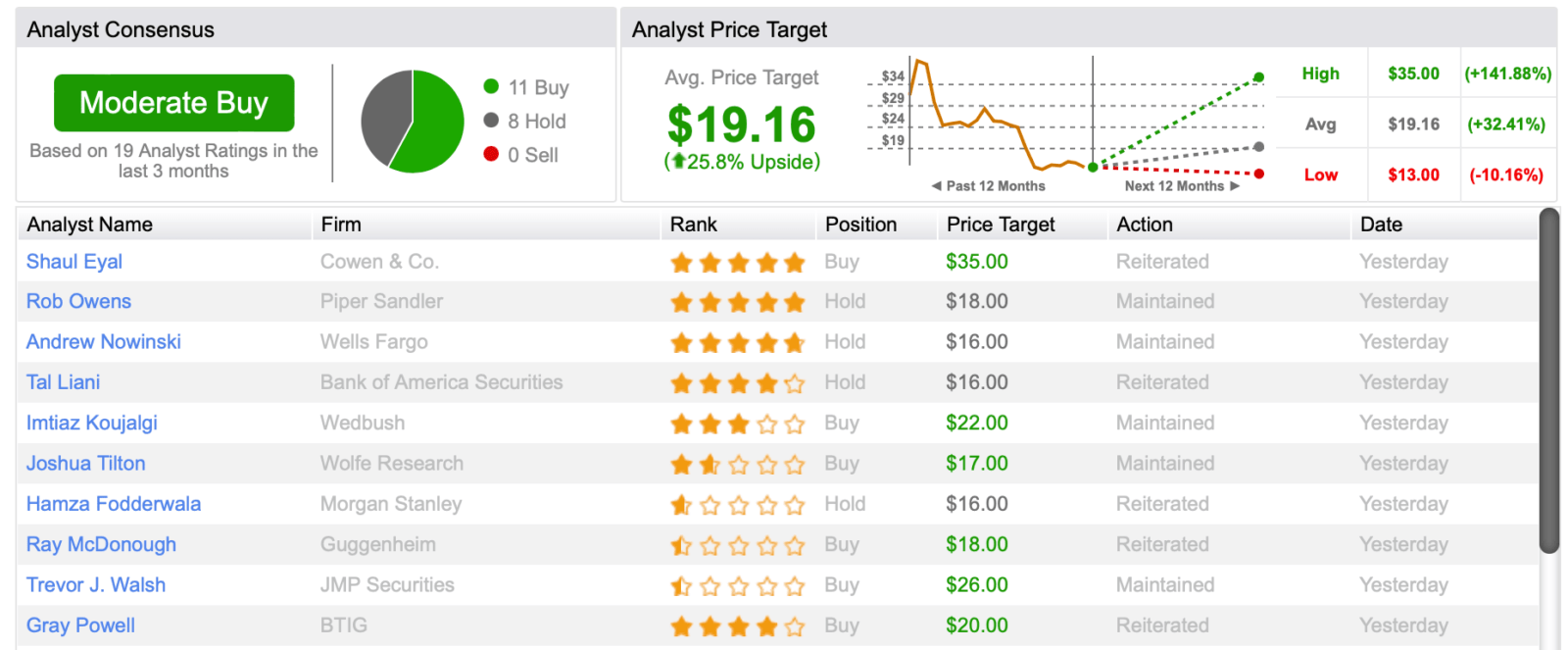

Analyst estimates:

It seems that analysts can’t decide between buy or hold. Because it still burns a lot of cash, has a high SBC, and slowing growth. But most of the time, they just change their price targets based on the price action. So I don’t really trust their targets or decisions.

Technicals:

It seems there’s good support at around $12 and strong resistance at $18.

❖ NET

Expected: $277

Results: Decent numbers, great guidance

Concerns:

- Will they achieve the FY guidance or are they trying to please investors?

- Do they really need to call their products based on others (R2, Descaler), why can’t they just show results and be done with it?

Decision: Sold some shares when price got over $70 as I felt that guidance might be an exaggeration and at that levels the stock is priced for perfection.

Risks:

Competition is stiff (taken from 10-K):

Bulls vs bears:

| Bulls say: | Bears say: |

| Tailwinds behind its back as edge computing becomes more prevalent | In direct competition with well-established, far larger incumbents such as Amazon, Microsoft, and Google |

| Security business is set to grow at a fast clip due to the overall security spend of enterprises going up as they deal with more complex security issues | GAAP unprofitable and may not achieve GAAP profitability for a few more years |

| Has a long runway for growth in terms of enterprise penetration in its security business | The CEO is a hugely influential person. If he were to leave or retire, future strategy and execution could suffer. |

Analyst estimates:

Technicals:

Moving on.

⓷ Trades & portfolio allocation

As of this writing my cash position is 0%.

I wish I could tell you whether or not we are at the bottom. But I’m not gonna do that. Here’s exactly what I own at the time being:

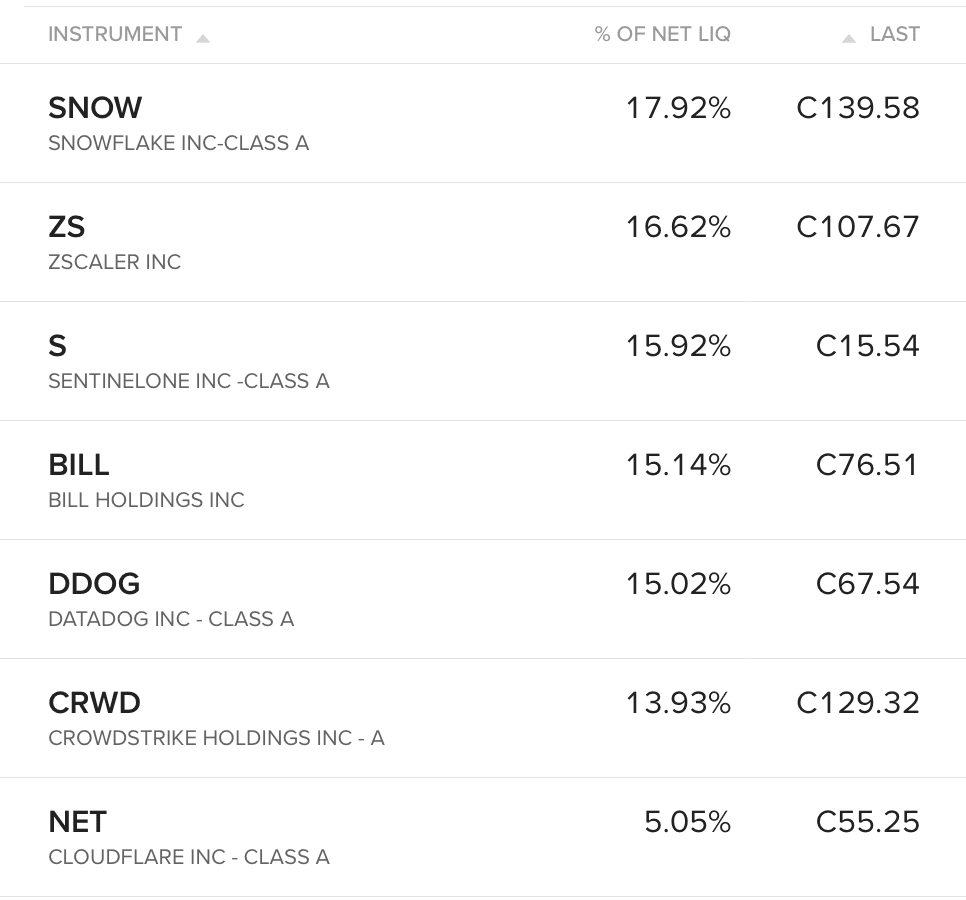

❖ Current positions

❖ Trades

This is when I added or trimmed my positions during the last few months (along with my reasoning for doing so):

◆ SNOW

I sold a few shares when it got to $170-175 because I felt like the odds were against us going into the earnings with that price.

After going through the report and listening to the call I bought back a few of the shares I had sold as I felt the market overreacted to the change in guidance and that was a fair price to pay for Snowflake.

◆ ZS

After the drop in the latest earnings, I bought a few extra shares as I feel there’s still a lot of growth for Zscaler even with the lower billings.

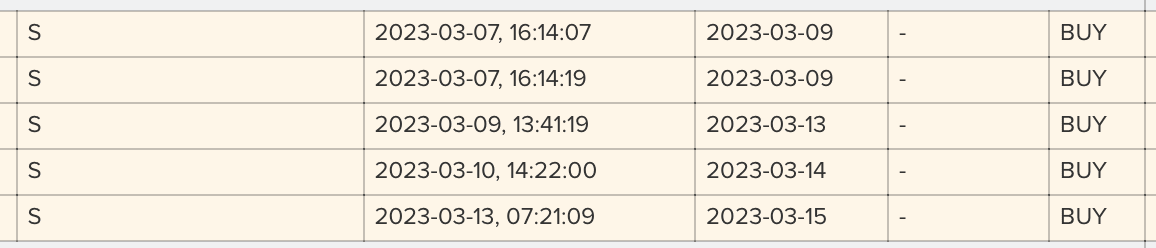

◆ S

I sold S when it got above $16 before the earnings to buy more ZS.

A few days later when the price dropped I added back all the shares and bought even some more before the earnings.

◆ BILL

I bought Bill.com as I felt the reaction from the Silicon Valley Bank collapse was too much. After reading the press releases (and confirming with IR that it won’t have a great impact on their financials) I added to my position.

◆ DDOG

I sold a few shares when it got above $90 as I felt the macro environment won’t let stocks run because there is (and will be for the foreseeable future) a slowdown. Hence valuations might come down and give us another opportunity to enter lower.

Once the shares started going below $70 I started adding them back because I feel at this price there is still a margin of safety even if the company slows down as low as reported (25%).

◆ CRWD

I went into the earnings with around a 10% position and liked what I read so I bought some more after hours and then again a few days later when it dropped to $118.

◆ NET

I started trimming when it got above $70 as I felt the stock was priced for perfection at that level. I’ll start adding more when/if it starts dropping below $50 (ideally at $40-45)

Next.

Final thoughts

My take is that 2024 won’t be the year of reacceleration. But the year in which investors pay a premium for companies that can maintain growth for longer. Since growth might be hindered now and pushed out even further.

Or maybe it was all pulled forward and that was it? I don’t think so. Because data suggest otherwise.

Cloud migration and digital transformation might have headwinds over the next Qs. But there’ll be tailwinds again in the future. The risk is that companies can’t say when at the moment.

And instead of reaccelerating from 30% to 50%, maybe they’ll just grow at 25%-30% for longer. And the end result will still be the same. And this is why long-term goals are still reiterated by several companies (NET, SNOW).

The question is: Are they just trying to play catch up and reassure investors? Or are they really confident about achieving their long-term goals? Time will tell.

Of course, everybody would want to be Madoff who “never” lost a trade. But I’m the first to admit I make plenty of mistakes. And I’ve said this many times before. But I’ll say it again.

The point is not to always be right. The point is to know why you are right (when you are right) and learn from your mistakes (when you are wrong).

I try to make decisions by reading reports and listening to calls before I read other people’s thoughts. This way I know my actions are based on my own thoughts. And what you read is my own.

So you may benefit (or not) but at least it’s original. And this is the only way to help each other. By writing original thoughts. Yes, I might sometimes change my mind if I read something that I missed or an opinion that made me really change my idea.

But most of the time I just stick to ’em. The more I make my own decisions the better I feel at night. And so will you.

The good thing about being able to make our own decisions is not only to avoid blaming others if something goes sour (that is still a valid reason), but also to really push ourselves to learn more, improve, and keep pushing forward.

This is a never-ending game. Constantly learning along the way. Even in the last 3 years, we’ve seen different strategies winning. Going from meme stocks, SPACs, and crypto to growth at all costs to FAANG, energy, value (whatever that means), and everything in between.

But in the end, everybody makes what helps them sleep at night. It’s your money. So act accordingly.

2020 might be the worst year for beginner investors. Because they got used to a fake reality. You could literally close your eyes, throw a dart at S&P 500 (to pick a company), and double your money.

Now, this is not what happens usually (as we’ve seen). And this set most investors up for failure. Because you see, when there’s a flood of money coming in, people just throw it around and keep pushing prices higher and higher (no matter the fundamentals).

Of course, the best names will always attract more money (but not at any price). And when the music stops, the ones who are left behind (just like in a Ponzi scheme) will lose the greatest.

When it comes to investing there’s no such thing as a derisked investment.

Anybody who says so is trying to sound smart (or stupid) or take your money. There’s always a risk/reward in everything. And as investors, this is the first thing we need to consider. Each and every single time.

When is this going to end? In other words, when are we gonna make some real money? My take is that stocks will jump when the Fed pivots (or when it’s expected to do so). When I say pivot I mean when they start cutting rates.

As they said this won’t happen before 2024 (but let’s see what happens now that several banks have collapsed). However, the stock market is always forward looking so the jump might happen earlier.

My only question is: Will companies perform better (reaccelerate) once that happens? Probably not as there’s always some lag as we’ve seen.

So even if the market gets excited with the Fed pivot, will they still punish or be more forgiving when companies report earnings that are still somewhat not ideal?

This keeps me invested at all times. And only add or trim when the risk/reward seems (to me) that is in (or against) our favor.

I don’t necessarily jump from one to the other like back in 2020-21 when I was just trying to catch the fastest horse. I still believe in the long-term prospects of these companies.

And I believe the market is making the assumption that these companies will become 10-20% growers next year and then just flat out. I’m not saying that 10-20% might never happen for some of these even for the foreseeable future. But I believe that companies are super prudent in their guide.

And even if they take another hit (decelerate further) they’ll keep operating for years to come. So the current multiples are justified for today’s performance. But I believe these companies will keep growing.

Yes, we left the early days of SaaS and cloud. But I believe with AI coming into play there will be significant growth down the line too.

In my view, selling out of ZS, DDOG, or SNOW just because they are slowing down at these levels makes no sense. Unless you have something growing faster (at a decent level/size) with a high probability of maintaining that for the long term (not just for this or the next quarter).

Everybody says market timing is a bad omen (something bad waiting to happen). But at the end of the day, we all just try to time the market, to find out winners, innovators, and those who have a head start in a specific industry. And so forth.

Having cash at times like this is great. As it gives you the chance to buy. A couple of quarters ago I started shifting from DCAing into positions to just adding when the risk/reward makes sense. As mentioned earlier, I’m currently at 0% cash (do with that what you will).

That’s all folks. Enjoy your day. And remember: investing (or trading) is just a part of our life. Not our entire life. Time is more important than money. Ask anyone with a boatload amount of money (but running out of time). They’ll tell you.

More from thoughts.money

Stocks Are Nothing like Groceries (Nor Perfume)