This article unveils the strategy to achieve sufficient wealth for a ten-year retirement.

At thoughts.money, various topics are discussed, including investment basics, money-saving lifestyle adjustments, income-generating entrepreneurial concepts, and a mindset that transforms these changes into positive choices rather than sacrifices.

Moreover, the internet provides retirement calculators, differing opinions from numerous financial advisors and pessimistic financial forecasts, unpredictable inflation, and diverse income-spending patterns among readers.

Amidst this flood of information, individuals often feel inundated and express sentiments like, “Yes, it’s commendable that people have retired at 30, but how can I accurately gauge the timeframe needed for my retirement, considering my distinct lifestyle?”.

Surprisingly, there’s a single key factor determining your path to retirement:

Your savings rate, shown as a portion of your take-home pay.

To simplify further, this savings rate depends entirely on two factors:

- Your yearly earnings.

- Your livable expenses.

Though these numbers are intuitive and easy to grasp, their connection can be eye-opening.

If you’re spending 100% (or more) of your income, retirement readiness remains out of reach. Unless someone else is saving for you (like well-off parents, social security, pension fund), you’ll continue working indefinitely.

Conversely, if your expenses are 0% of your income (living entirely cost-free) and you can sustain this in retirement, immediate retirement is feasible. This makes your working years zero.

Between these extremes lie intriguing factors. When you start saving and investing, your money begins generating income on its own. These earnings then generate more earnings. A compounding cycle of income unfolds rapidly.

Once this income covers your living costs and allows gains to be reinvested annually to match inflation, retirement becomes viable.

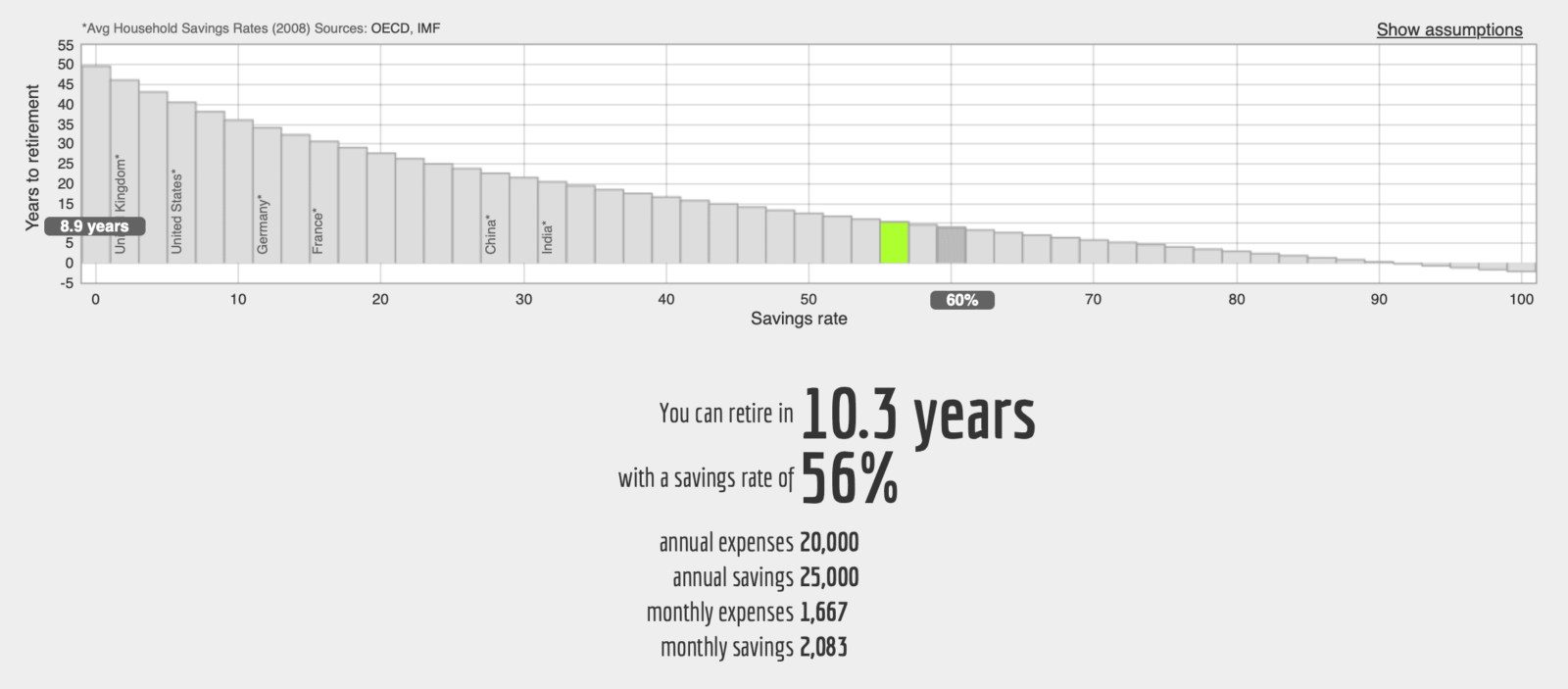

If you were to illustrate this “savings rate” concept on a graph, it wouldn’t be a linear line; instead, it would take the form of a smooth, curved exponential graph, like so:

You can go to Networthify and play with the numbers and see what fits you best.

If you set aside a sensible portion of your take-home pay, say 56%, and use the remaining 44% for your expenses, you’ll reach a state of being “financially independent” in a reasonable timeframe – roughly around 10.3 years as indicated by this chart.

Now, let’s simplify the graph mentioned earlier. Here are some cautious assumptions, enabling you to concentrate on saving the largest proportion of your take-home pay possible. The table below will give you a rough estimate of how many years it might take for you to achieve financial independence.

Here are the underlying assumptions:

- You can achieve 5% investment returns after adjusting for inflation throughout your saving years.

- After retiring, you’ll rely on the “4% safe withdrawal rate” for your living expenses. There will be some adaptability in your spending during economic downturns.

- You intend for your investment portfolio to last indefinitely. You’ll only use the gains, ensuring this income supports you for a period of around seventy years. Think of this assumption as a comfortable and cautious margin of safety.

Below is the breakdown of the number of years you would need to work, given various potential savings rates, commencing from a net worth of zero:

| Savings Rate (Percent) | Working Years Until Retirement |

|---|---|

| 5 | 66 |

| 10 | 51 |

| 15 | 43 |

| 20 | 37 |

| 25 | 32 |

| 30 | 28 |

| 35 | 25 |

| 40 | 22 |

| 45 | 19 |

| 50 | 17 |

| 55 | 14.5 |

| 60 | 12.5 |

| 65 | 10.5 |

| 70 | 8.5 |

| 75 | 7 |

| 80 | 5.5 |

| 85 | 4 |

| 90 | Under 3 |

| 95 | Under 2 |

| 100 | Zero |

This phenomenon is truly remarkable, especially towards the less frugal end. A middle-class family earning $50,000 in take-home pay and saving 10% ($5,000) is surpassing the average these days. Yet, regrettably, being “better than average” still falls short, requiring around 51 years of work.

However, a simple act like cutting cable TV and a few coffee shop visits would instantly push their savings rate to 15%, enabling them to retire years earlier. Are these luxuries worth the extra years of work?

The paramount observation is that reducing your spending rate holds more potency than boosting your income. This is because every lasting cut in expenses yields a dual impact:

- More money is available monthly for saving.

- Your monthly requirement diminishes permanently, sustaining you for life.

Hence, your passive income over your lifetime increases due to a larger investment pool. Plus, it more comfortably meets your needs as your skill in efficient living grows, reducing your necessities.

If a 10-year retirement is your goal, the formula is right there: live on 35% of your take-home pay.