| Key Information | Details |

|---|---|

| Latest Earnings Report | Global-e’s recent earnings report surpassed expectations, exhibiting higher revenue and adjusted EBITDA compared to projections. |

| Growth Drivers for 2024 | The company’s growth prospects for 2024 are driven by the Shopify Markets Pro platform and the transition of Borderfree customers to its proprietary platform. |

| Business Model and Cost Ratios | Global-e’s business model has shown notable enhancements, with increased gross margins and consistent operating expenses. |

| Leadership in B to C Cross Border E-commerce | The company holds a dominant position in B to C cross-border e-commerce, which is projected to expand tenfold by 2030. |

| Customer Acquisition and Pipeline | Global-e achieved unprecedented levels of new customer acquisitions and maintains a record pipeline for the second half of 2023. |

What you'll learn:

☞ Shall You Invest in Global-e Now?

| Pros of Investing in Global-e | Cons of Investing in Global-e |

|---|---|

| Strong Revenue Growth: Global-e has consistently shown strong revenue growth, with a projected mid-high 30% CAGR over the next few years. | Market Volatility: Like any investment, Global-e’s stock can be influenced by market fluctuations and external factors. |

| Strategic Partnerships: The partnership with Shopify provides access to a wide customer base and potential growth through Shopify Markets Pro. | Limited Operating History: Global-e is a relatively new company, and its limited operating history might make it harder to accurately predict its long-term performance. |

| Unique Market Position: Global-e offers a holistic solution for brands and merchants looking to enter the cross-border e-commerce market, positioning itself as a leader in a growing industry. | Competition: The e-commerce space is competitive, with major players like Amazon, Alibaba, and eBay. Global-e’s ability to maintain its market position will be crucial. |

| Impressive Margin Performance: The company has demonstrated consistent margin improvement, indicating effective cost management and operational efficiency. | Macro Economic Factors: Economic conditions can impact the company’s growth, especially considering its exposure to international markets. |

| Favorable Cost Ratios: Global-e has shown improvement in gross margins and operating expenses, contributing to a positive profitability trend. | Uncertainty of Markets Pro Impact: While Markets Pro offers potential, the exact impact on Global-e’s growth and profitability remains uncertain. |

| Growth Potential: The cross-border e-commerce market is forecasted to grow significantly, offering ample room for Global-e’s expansion. | Transition Challenges: The migration of Borderfree customers to Global-e’s platform might pose short-term challenges in terms of revenue growth. |

Global-e (NASDAQ: GLBE) shares have experienced a surge since late 2022. However, the recent earnings release and guidance, although positive, didn’t prevent a modest valuation consolidation.

Despite this, there’s renewed optimism due to stronger growth, improved profitability, and a compressed stock price.

During the second quarter earnings season, many IT stocks faced consolidation. Higher long-term interest rates, rising to around 4.29% in three months, contributed to this trend. Factors behind this rate increase include shifting perceptions of a recession and evolving macro expectations based on PMI data in the US and the EMEA region.

Bond yields rose following a robust retail sales report and moderately hawkish Fed commentary in the latest Fed Minutes. Oddly, the impact of China’s weak economy on demand hasn’t been fully considered. China’s subdued demand affects areas from shipping to energy and metals.

This article doesn’t discuss long-term rate expectations. Elevated real rates, as seen now, influence demand for long-lasting assets like homes, cars, and capital goods. Capital goods demand is showing early signs of change, while consumer durable demand, including housing starts, remains steady despite lower builder sentiment.

As long as long-term rates remain high and rising, they could limit the value of high-growth IT shares. This situation has been evident in recent weeks.

Thus, it seems sensible to focus on companies with positive fundamental shifts but declining stock prices. Global-e fits this profile, warranting a closer look from readers and subscribers.

☞ Strong Quarter, Conservative Guidance

In this earnings season, most high-growth IT companies have faced challenges. Valuations compressed due to various factors, and many companies struggled to meet investor expectations in their guidance. Despite economic resilience, the growth achieved in 2021 and early last year hasn’t fully returned. Stability and moderate improvement are the current trends.

Amidst this, Global-e stands out. While primarily an e-commerce player, the company’s revenue increasingly comes from software localization services and other e-commerce elements it provides. Investors are more interested in the company’s consistent ability to surpass expectations rather than categorizing it.

Initially, Q2 projections were $770 million in gross merchandise value (GMV) and $3,480 million for the year. Revenue for the reported quarter was estimated at $128 million, and full-year revenue at nearly $580 million. Though non-GAAP EPS isn’t explicitly forecasted, adjusted EBITDA provides a basis for this metric. The company forecasted around $17 million adjusted EBITDA for the quarter and raised its forecast going into Q2.

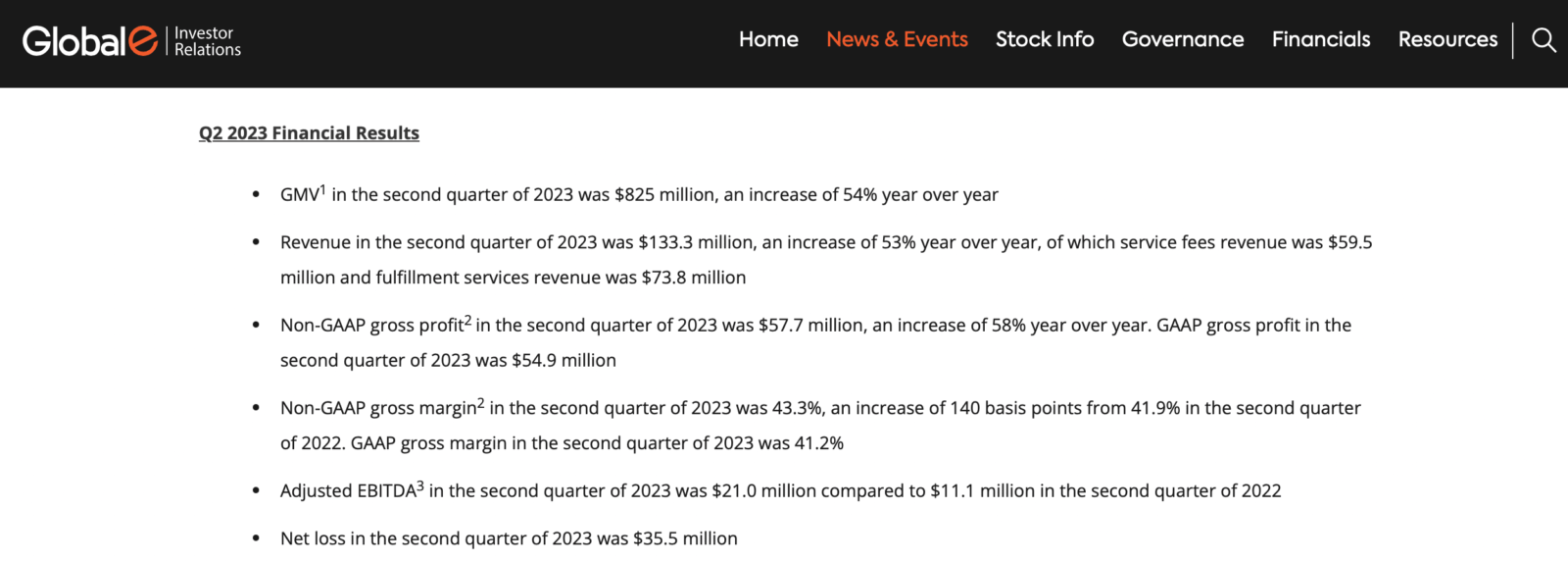

Q2 results exceeded forecasts: GMV reached $825 million (+7%), revenue hit $133 million (+4%), and adjusted EBITDA reached $21 million (+25%).

Revised full-year forecasts: GMV expected at $3,560 million (+2.3%), revenue at about $585 million (+2%), adjusted EBITDA projected around $90 million (+20%).

Amid the current macro environment, any positive guidance is noteworthy. Global-e noted accelerated growth in 2H, highlighting Shopify Markets Pro as a contributor. The company’s conservative forecasting has been consistent since going public.

Regarding 2H, Global-e foresees some growth challenges from the acquired Borderfree business. The integration of Borderfree customers into its platform is ongoing, and slower expansion may impact revenue growth by a few basis points before migration to Global-e’s direct-to-consumer platform creates synergies.

A key reason to consider buying shares now is the anticipated growth in the next year. This growth stems from Borderfree customer migration and the rising traction of the Shopify Markets Pro platform throughout 2024 and beyond.

☞ What Are Global-e’s Growth Catalysts?

Global-e is set to capitalize on substantial growth opportunities in 2024, with three major drivers propelling its expansion: Market Pro, Borderfree, and a new range of customers.

Analysts predict a remarkable 37% organic revenue growth for Global-e in the upcoming year, which ranks among the highest projections in the companies being monitored. This ambitious growth forecast requires careful evaluation to gauge its realistic potential and its impact on valuation.

Recent periods have seen outstanding growth from outbound US brands, achieving a noteworthy 99% growth last quarter. While a part of this stems from the Borderfree merger, it’s important to note that the acquisition of Flow Commerce, a factor in prior quarters, did not contribute to this latest quarter’s growth due to the acquisition’s lapping.

Brands with strong franchises, particularly celebrity brands, have been driving substantial GMV growth compared to others.

Though the 99% growth rate is unlikely to persist into 2024, the outbound US segment is expected to outpace the company’s overall growth, mainly driven by Shopify Markets Pro.

Global-e currently boasts a record pipeline and substantial new deal signings in the first half of the year, with guidance based on these signed deals. The transition of Borderfree customers to its platform and strategic marketing initiatives are anticipated to create growth tailwinds in 2024.

While Global-e’s existing customer GMV expansion has been around 30% per year, this is adjusting due to the inclusion of customers acquired from the Borderfree acquisition, which have shown lower expansion rates. The ongoing migration of previous Borderfree users to Global-e’s platform is expected to enhance the expansion rate in the latter part of 2024 and into 2025.

Global-e’s strategic partnership with Shopify holds significant value, with a commercial agreement featuring both development and sales collaborations. The upcoming Shopify Markets Pro holds immense potential, providing a localized white-label version of Global-e’s offering. This allows merchants to sell directly to consumers with localized websites and streamlined administrative processes.

The revenue split between Shopify and Global-e remains undisclosed, but Markets Pro offers a unique value proposition for Shopify’s merchants. This service, with its modest costs, is poised to attract a substantial number of merchants seeking to tap into international markets with ease.

The launch of Markets Pro has been gradual, with positive feedback from initial users. Improvements in onboarding and day-to-day management are ongoing, with a wider rollout expected in the future.

As Markets Pro gains traction, it’s speculated that it could contribute a notable portion to Global-e’s revenue, potentially adding $80 million to $100 million. The exact extent of this impact remains uncertain, with “substantial” being the most accurate description at present.

The advent of Markets Pro and other growth drivers holds the potential to reshape Global-e’s revenue streams and further amplify its prominence in the e-commerce landscape. As this journey unfolds, both investors and industry observers eagerly await the company’s strategic moves and their subsequent impact on its trajectory.

☞ How Is Macro Affecting Global-e’s Growth?

The lingering question about the extent of economic macro headwinds impacting Global-e’s growth has been on investors’ minds. However, there’s no straightforward answer to either dismiss or overly emphasize macro factors in the company’s outlook.

Global-e is a relatively small entity operating in a vast market. Its current market penetration is low enough that it can continue growing even if broader e-commerce faces macro-related challenges.

It’s noteworthy that macro conditions don’t seem to be significantly hindering GMV growth for major players in the e-commerce space. While macro headwinds are a factor to consider, they are unlikely to be the sole determinant of the company’s growth rate.

Recent European economic PMI reports have indicated weakness, yet Global-e’s performance in the EMEA region appears stronger than other areas. This suggests that despite macro conditions, the company’s operations in this region have remained resilient.

The historical expansion rate of existing brands might decrease in the coming year, but this could be overshadowed by record new customer acquisition and a strong pipeline. In a slow-growth setting, brands not yet engaged in international sales might turn to direct-to-consumer approaches, particularly with services like Global-e that eliminate the need for substantial upfront investments.

The impact of Markets Pro on next year’s GMV is crucial, and the current forecast already factors in a notable growth deceleration from non-Markets Pro channels. This suggests that growth could be around 25% for revenues next year, compared to the high 30% range this year.

Overall, the consensus forecast for next year’s revenue growth doesn’t seem to carry significant risk from worse-than-expected macro conditions, based on current assessments.

☞ Who’s Global-e’s Competitor?

Numerous vendors enable direct-to-consumer e-commerce, but many offer only partial solutions instead of comprehensive end-to-end platforms. A third-party assessment of alternatives to Global-e reveals a variety of companies focusing on specific areas such as international payments, fraud prevention, tools, APIs, and shipping services.

Among these, the closest competitor is the French company Glopal, which concentrates on French luxury brands and employs a composable element approach similar to Shopify’s strategy for attracting new customers.

The global e-commerce market is still in its infancy. An industry analyst estimates that the Gross Merchandise Value (GMV) could surge to $71 trillion by 2028, up from less than $17 trillion in the previous year, projecting a Compound Annual Growth Rate (CAGR) exceeding 28%.

In terms of significant competition, companies like Amazon, Alibaba, eBay, and Walmart are prominent players. Many brands prefer to sell their products directly to large retailers rather than directly to international consumers. This applies to local retailers too, who have a strong presence in a specific geographic area but lack international recognition.

According to a survey, cross-border business-to-consumer e-commerce, the domain of Global-e, is projected to grow over 10-fold by the end of the decade. The estimated GMV by 2030 is anticipated to reach approximately $8 trillion. While these figures are subject to uncertainty due to the evolving nature of this market, it’s clear that the potential is substantial.

With minimal market penetration so far, Global-e holds a leadership position with its comprehensive solution. The collaboration with Shopify further reinforces the company’s dominance in the market.

☞ What’s Global-e’s Business Model Like?

Global-e operates as more than a software company. It provides a comprehensive direct-to-consumer solution for brands and merchants aiming to expand internationally. Evaluating its business model and cost dynamics involves different considerations than those for pure software vendors. Distinctive in its offering, Global-e lacks direct analogs, adding to its appeal.

The latest quarter revealed a surprising upswing in non-GAAP gross margins. With revenue reported in two segments – services and fulfillment – the mix has been shifting toward services, resulting in gross margin expansion. While the Borderfree merger influenced the mix trend last quarter, non-GAAP gross margin rose to 43.3%, a notable improvement.

Service fee revenue increased by 51% YoY, while fulfillment service grew by 54%. Despite fulfillment accounting for 55% of revenue and services 45%, non-GAAP gross margin improved to 43.3%, up from 41.9% in the prior quarter.

The 140 basis point increase defied expectations. Factors contributing to this growth were not extensively elaborated by the company CFO, though a continued margin increase is expected, albeit at a more moderate pace.

Other expense ratios displayed positive trends. Sales and marketing expenses rose modestly year-on-year and remained flat sequentially. General and administrative expenses decreased by about 7% YoY and slightly sequentially. Research and development expenses increased as the company invested in launching Markets Pro, surging 41% YoY and 7% sequentially.

On a GAAP basis, operating expenses rose by around 10% YoY and 4% sequentially. Excluding stock-based compensation, the operating margin remained negative. Adjusted EBITDA margin increased to 16% last quarter, up from 13% the prior year. The company’s projection for a 16% full-year EBITDA margin indicates consistent margin improvements.

While Global-e had a negative free cash flow margin over the past six months, free cash flow significantly improved last quarter. Adjusted EBITDA margin and free cash flow margin are anticipated to converge over time. Global-e also operates as a payment company, leading to varying fund payable balances to customers.

As Markets Pro gains prominence in Global-e’s revenue mix, services are expected to grow as a percentage of the total, potentially boosting gross margin percentage. The impact of Markets Pro on operating expenses remains uncertain, though the revenue line is likely to be more profitable than average.

Stock-based compensation (SBC) expense decreased to 8% of revenue from 15% YoY. Outstanding shares increased by 4.4% YoY and 1% sequentially, with an estimated average of 170.5 million shares over the next year.

Estimating margins for a company with projected mid-high 30% growth is challenging. Opex remained stable last quarter and moderately increased YoY, with no indications of reaccelerating growth.

Should revenues grow 37% (consensus forecast), opex 10%, and gross margins improve slightly, EBITDA margin estimates might be conservative. Caution is advised in projections, though potential upside exists if strategies and Markets Pro release align well.

☞ Final thoughts on Global-e

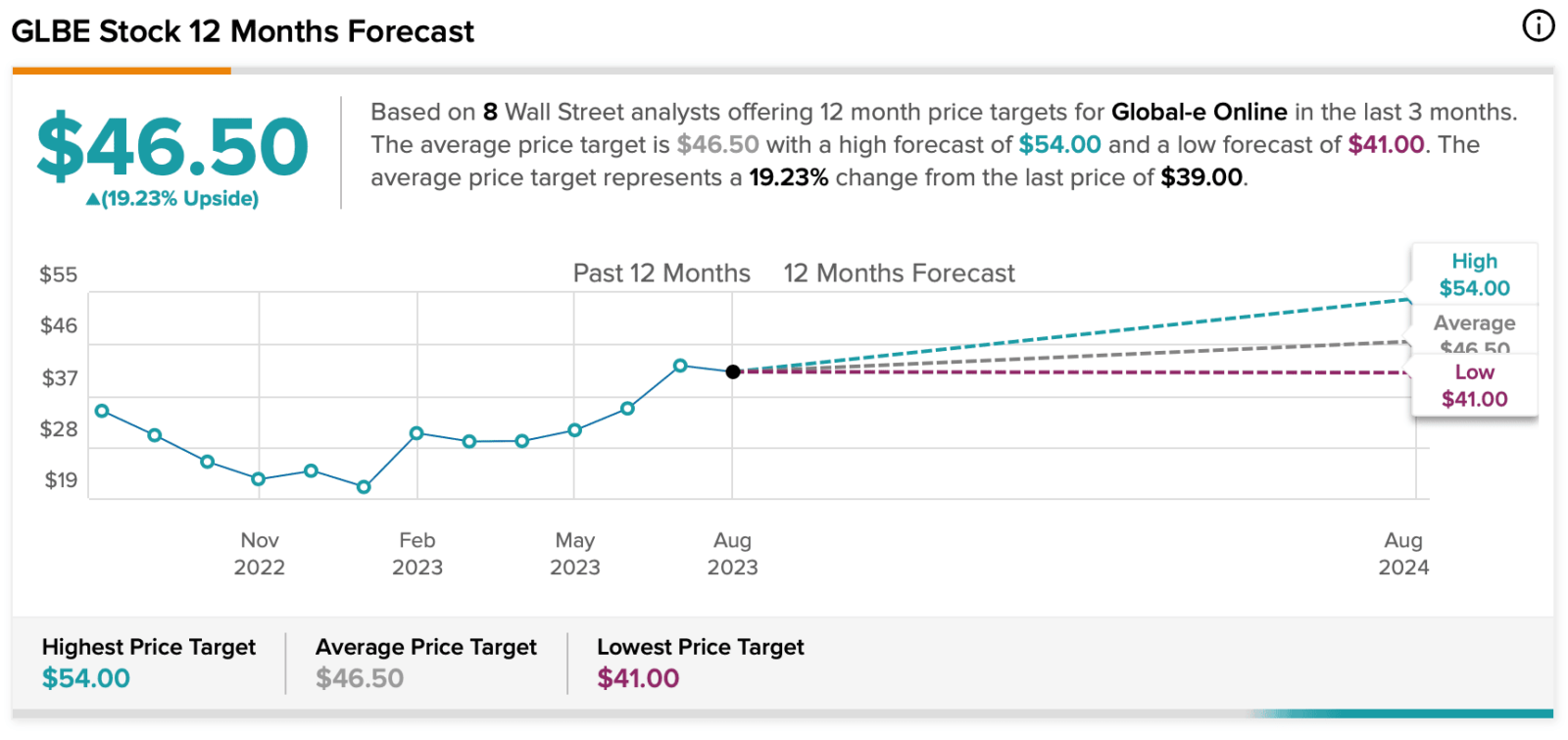

Global-e’s forward EV/S ratio of about 8.5X is above average considering its projected mid-high 30% 3-year CAGR, potentially even higher with Markets Pro’s impact. However, its valuation appears below average when considering its estimated low 20% free cash flow margin over the next year. Despite a Rule of 40 metric nearing 60, the valuation doesn’t fully reflect growth and profitability.

The expansion opportunity in Global-e’s market is substantial, with forecasts of a 10X growth over the decade. Though skeptical due to the lack of historical precedent, the opportunity is immense for Global-e in the cross-border e-commerce space.

The partnership with Shopify is pivotal, contributing to about 15% of Shopify’s GMV from outside North America. The newly released Shopify Markets Pro, a cornerstone of the partnership, offers potential, though its impact remains uncertain. Some analysts estimate the partnership could contribute 1000-1500 basis points to a 37% consensus growth forecast next year, but this remains speculative.

Impressive margin performance has surprised many, particularly in gross margins, resulting from fundamental improvements. Short-term guidance is cautiously optimistic, considering headwinds from transitioning Borderfree users to Global-e’s platform.