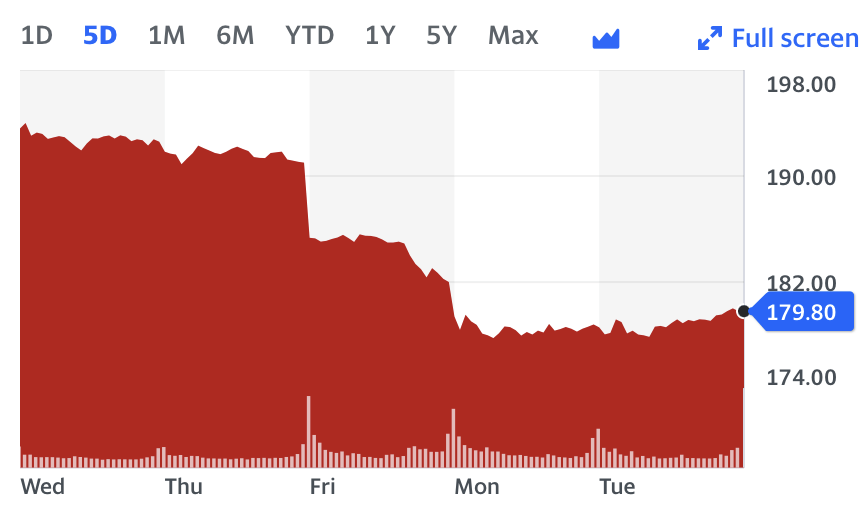

Apple, the tech giant known for its innovative products, has experienced a significant drop in its market value, losing over $200 billion in less than a week. This downturn comes in the wake of its recent earnings report, revealing challenges in its core business segments. Let’s delve into what has led to this market turbulence.

Image Source: Yahoo Finance

What you'll learn:

➤ Earnings Disappointment

The upheaval began on August 3rd when Apple reported disappointing iPhone sales for the June quarter, causing its overall revenues to decline by 1% year-over-year to $81.8 billion. Despite its success in growing its services division – which includes the App Store, iCloud services, Apple Music, Apple TV+, and Apple Pay – iPhone sales still make up approximately 50% of its total revenue. This dependence on iPhone sales triggered a wave of analyst downgrades, reflecting concerns about Apple’s performance.

Rosenblatt analysts lowered their rating from “buy” to “neutral,” indicating that the company is facing a “slowdown phase.” Similarly, Loop Capital analyst Ananda Baruah adjusted the rating from “buy” to “hold,” citing the risk to Apple’s revenue guidance if iPhone sales do not recover throughout the year.

The quarter proved challenging for Apple’s hardware sales across the board. iPhone revenues decreased by 2.4% year-over-year to $39.7 billion, Mac revenues dipped by 7.3% to $6.8 billion, and iPad revenue experienced a significant decline of 19.8% to $5.8 billion.

➤ Weak Outlook

Further contributing to the recent decline in Apple’s stock is a weaker-than-anticipated guidance from the company’s management. Apple projected gross profit margins of 44% to 45% for the September quarter, with potentially stagnant or slightly slower year-over-year revenue growth. The Chief Financial Officer, Luca Maestri, expressed expectations of continued revenue declines for the Mac and iPad throughout the year, despite a potential acceleration in iPhone and services segment revenue.

Prominent Wedbush tech analyst Dan Ives acknowledged that the guidance fell short of market expectations. Additionally, Bank of America analysts underscored the weak U.S. smartphone market as a backdrop for Apple’s outlook.

➤ Valuation Concerns

Analysts also highlight Apple’s lofty valuation as a factor pressuring its stock. Despite consecutive quarters of declining revenue, Apple’s shares surged by 51% year-to-date at their peak, resulting in trading multiple as high as 33 times earnings. Even after the recent post-earnings stock price decline, Apple’s valuation remains approximately 30 times earnings. In comparison, the broader S&P 500 index trades at around 20 times earnings.

While some analysts emphasize Apple’s cost-saving efforts and robust high-margin services revenue, others express concerns about its heavy reliance on diminishing iPhone sales in a challenging macroeconomic environment.

➤ Mixed Market Sentiment

Despite the recent market turbulence, Wall Street analysts’ responses to Apple’s situation vary. While concerns persist about declining iPhone sales indicating reduced demand for the company’s primary product, optimistic analysts highlight that, on a constant currency basis, revenues from the iPhone segment actually grew by 1.4% year-over-year last quarter.

Wedbush tech analyst Dan Ives argues that foreign currency exchange headwinds were the main factor affecting iPhone revenues’ performance, and he anticipates a “mini super cycle” of demand upon the release of the iPhone 15 in September.

➤ Long-Term Prospects and Caution

Many analysts maintain a positive long-term outlook for Apple, despite recent challenges. These optimists point to Apple’s strong performance in key overseas markets, including an 8% year-over-year rise in China iPhone revenues and record-high iPhone revenues in India.

Bank of America analyst Wamsi Mohan suggests that Apple’s services business revenue could continue growing due to improving trends in areas such as advertising, mobile gaming, and App Store sales. He also highlights a notable increase in “switchers” to iPhones in China.

Nonetheless, not all analysts share this optimism. Some express concern over Apple’s premium valuation compared to the broader market. UBS analyst David Vogt emphasizes that the company trades at a roughly 50% premium to the S&P 500, and he believes that challenging conditions in the smartphone market could continue to impact the stock.

While differing opinions exist, Apple’s ongoing efforts to navigate these challenges and capitalize on its diverse revenue streams will be crucial in determining its future trajectory.

(Original article source: Fortune.com)

➤ This Is What People Say:

| Reader Comments |

|---|

| The recent stock drop seems more like profit-taking and human behavior than a reflection of Apple’s business performance. Optimism prevails that Apple will regain its value soon. |

| Apple’s stock fluctuations are typical for the market. Comparisons to Enron are unfounded, emphasizing Apple’s solid financial position. |

| An amusing take on Apple’s product trends, suggesting excessive features like multiple cameras and chargers. |

| High iPhone prices lead to longer product retention, with minimal groundbreaking upgrades in recent generations. |

| Apple’s high prices and economic uncertainties influence consumer decisions to update devices. |

| The potential impact of overpriced VR products on Apple’s performance is questioned. |

| Apple’s technological innovation is criticized, while Android phones are cited as more widely used globally. |

| Android’s broader market presence is acknowledged, while Apple’s market share leadership in specific regions is highlighted. |

| Apple’s services, coupled with iPhones, create an attractive package. |

| The decline of Android’s market share against Apple is contested, emphasizing Apple’s profit dominance in the smartphone sector. |

| A metaphorical comparison between Apple and Android users is drawn. |

| A projection that sustainability concerns may impact components used in Apple products. |

| Competition and technological maturity are discussed, highlighting the attractiveness of alternative phone options. |

| Apple’s innovation post-Steve Jobs is questioned, while acknowledging Tim Cook’s role. |

| Suggestions for drastic changes in Apple’s iPhone pricing and development cycle are offered. |

| Apple’s high earnings are noted, suggesting a reconsideration of its stock price. |

| Short-term challenges are dismissed, with optimism for Apple’s recovery by year-end. |

| A satirical prediction of revolutionary features in iPhone 15. |

| Perceived overpricing of Apple products leads to exploring alternative, more cost-effective options. |

| A view that Apple’s innovation has stagnated post-Steve Jobs. |

| A simplified explanation for weak quarters due to consumer spending patterns is offered. |

| Apple’s innovation post-Steve Jobs is questioned, emphasizing the lack of revolutionary products. |

| Apple’s financial performance is acknowledged, with skepticism about its growth potential. |

| Investors’ cautious response to Apple’s premium stock price is highlighted. |

| A call for calm amidst concerns about Apple’s performance. |

| Comparisons to the overvaluation of Apple and the anticipation of another company’s potential decline are made. |

| Consideration of Android phones due to Apple’s perceived overpricing is discussed. |

| Apple’s challenges in competing in emerging markets due to high prices are mentioned. |

| A perspective on retail stock buyers’ perceptions and market realities is shared. |

| Motivations behind Chinese iPhone users are speculated upon. |